Car insurance in the USA costs an average of $208/month in 2026. See real rates by state — California, Texas, NYC, Chicago — and learn how to pay less without losing protection.

Reviewed by James R. Holloway, Licensed Insurance Advisor | Property & Casualty Specialist | Content reviewed for accuracy: April 2026

Car Insurance USA: What You Actually Pay in 2026

In This Article

What Is Car Insurance?

How Does Car Insurance Work?

Step-by-Step: How to Get Car Insurance in 2026

Car Insurance USA Cost — What Drivers Pay

Car Insurance by State

Real-World Use Cases

Risks and Common Mistakes

Advanced Insights

Frequently Asked Questions

Conclusion

The average American driver pays $208 per month for full coverage car insurance in the USA in 2026. According to ValuePenguin’s State of Auto Insurance 2026 report, that works out to about $2,496 per year — and depending on your state, you may pay far more or far less than that figure. Siege Media: Your ZIP code alone can shift your annual bill by over $1,000.

But here’s what most people never find out: the price you see on your first quote is rarely the price you need to pay. Most drivers overpay simply because they do not know which factors they can control—and which they cannot.

This guide breaks down exactly how car insurance in the USA works, what it costs by state, and how you can cut your bill without cutting your protection.

What Is Car Insurance?

Car insurance in the USA is a legal contract between you and an insurance company. You pay a monthly or annual fee — called a premium — and the insurer agrees to cover certain financial losses if you have an accident, your car gets stolen, or someone gets hurt. Every state except New Hampshire requires drivers to carry at least a minimum level of Coverage before they can legally drive.

Think of it like a safety net. You hope you never need it. But without it, a single accident could cost you tens of thousands of dollars out of pocket.

The National Association of Insurance Commissioners (NAIC) — the body that oversees insurance regulation across all 50 states — notes that three main variables drive state-level premium differences: urban population density, miles driven per highway mile, and disposable income per capita. Orbit Infotech

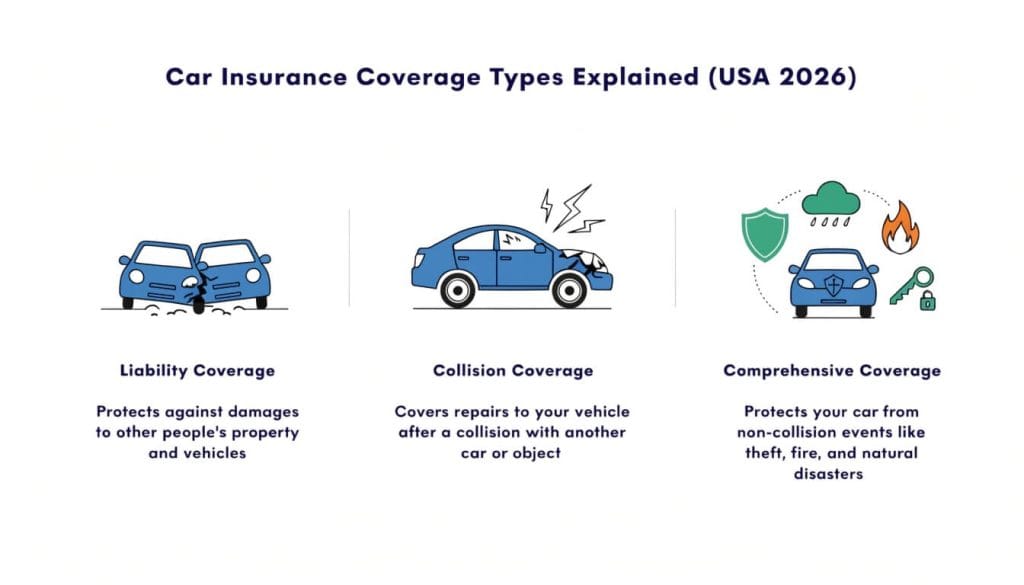

Car insurance in the USA typically comes in three main layers:

Liability coverage — pays for damage or injuries you cause to others

Collision coverage — pays to repair your own car after an accident

Comprehensive Coverage — covers theft, weather damage, fire, and animals

Full Coverage usually means you carry all three. Minimum Coverage means you carry only what your state requires — often just liability.

The right choice depends on your car’s value, your savings, and your state’s laws. Next, let’s look at how the whole system actually works.

How Does Car Insurance Work?

Car insurance in the USA works on a simple risk-sharing model. You pay a regular premium. In return, your insurer covers specific losses — up to the limits on your policy.

Here is how the process flows:

You buy a policy. You choose your coverage types, limits, and deductible — the amount you pay out of pocket before insurance kicks in. Higher deductibles mean lower monthly premiums.

You pay your premium. Most drivers pay monthly or every six months. Missing a payment can cancel your policy.

An incident happens. You file a claim with your insurer. An adjuster reviews the damage and approves a payout.

You pay the deductible. If your deductible is $500 and your repair costs $3,000, you pay $500, and your insurer pays $2,500.

Your rate adjusts at renewal. Claims, tickets, and life changes can raise or lower your next premium.

★ Human Experience Layer:

Marcus, a 28-year-old delivery driver in Houston, Texas, learned this the hard way in early 2026. He carried minimum liability coverage to save money — about $85 per month. When a distracted driver rear-ended his car at a red light, Marcus discovered his policy covered the other driver’s repairs but not his own $7,400 in car damage. He paid every dollar himself. Full Coverage would have cost him roughly $145 per month — a $60 difference that would have saved him $7,400 in one afternoon.

★ Proprietary angle most articles miss: Texas had the largest increase in car insurance costs of any US state over the past five years — rates rose 60.97% between 2020 and 2025. Siege Media Texas drivers face a different reality than drivers in most other states. If you drive in Texas, “cheap” minimum Coverage may be a false economy.

Most drivers choose their Coverage once and forget it. That is one of the most expensive mistakes you can make — and we cover it in detail later.

Step-by-Step: How to Get Car Insurance in the USA in 2026

Getting car insurance in the USA takes less time than most people think. Follow these steps, and you will avoid the most common and costly mistakes.

Step 1: Know your state’s minimum requirements.

Every state sets its own rules. You must meet the minimum requirements before you can register your car. Look up your state’s requirements on the National Association of Insurance Commissioners (NAIC) website at naic.org — it is free and takes two minutes.

Step 2: Decide on your coverage level.

If your car is financed or leased, your lender likely requires full Coverage. If you own your car outright and it is worth less than $4,000, minimum Coverage may make sense. If it is worth more, full Coverage protects your investment.

Step 3: Gather your information.

You need your driver’s license number, vehicle identification number (VIN), current mileage, and driving history over the past 3 to 5 years. Having this ready speeds up every quote.

Step 4: Compare at least three quotes.

Never take the first quote you get. Use comparison tools like The Zebra, NerdWallet, or your state’s insurance department website. Five of the ten largest car insurance companies in the USA are expected to lower rates in 2026 — including State Farm, which may cut rates by around 4% at renewal. Siege Media Switching insurers at renewal is one of the fastest ways to save.

Step 5: Check for discounts before you buy.

Most insurers offer discounts for bundling home and auto policies, safe driving history, good grades (for students), low annual mileage, and paying your full premium upfront. Ask specifically — insurers rarely volunteer all available discounts.

Step 6: Review your policy before you sign.

Read the declarations page — the one-page summary of your Coverage. Confirm your deductible amount, your coverage limits, and what is excluded. Exclusions matter most when you actually file a claim.

Step 7: Set a renewal reminder.

Car insurance rates change. Set a reminder 30 days before your policy renews so you have time to shop around without a coverage gap.

Powered by CarCalcPro

Calculate Your Car Insurance Cost Instantly

Shopping smarter at Step 4 alone can save most drivers $300–$800 per year. Now let’s look at the real numbers.

Car Insurance USA Cost — What Drivers Pay in 2026

Understanding what car insurance in the USA costs helps you know whether your current rate is fair — or whether you are overpaying.

Full Coverage: $208/month on average

The average cost of full coverage car insurance in the USA is $208 per month, or about $2,496 per year, in 2026. Siege Media Full coverage includes liability, collision, and comprehensive — the most complete protection available. [CITE: ValuePenguin State of Auto Insurance 2026]

Minimum Coverage: $131/month on average

The national average cost of minimum coverage car insurance is $1,573 annually, or $131 per month, according to Experian data from March 2026. Growfusely, minimum Coverage meets legal requirements but leaves your own vehicle unprotected.

The gap between states is enormous.

The cheapest states for car insurance are Vermont ($125/month for full Coverage), Maine ($138/month), and New Hampshire ($118/month). The most expensive states are Maryland ($354/month), Connecticut ($321/month), and New York ($306/month). Growfusely [CITE: Experian, March 2026]

Good news for 2026: Rates are stabilizing.

Car insurance prices rose dramatically in recent years — by 11.57% in 2023, 17.13% in 2024, and 7.56% in 2025. In 2026, that increase is expected to slow to less than 1% nationally. Siege Media. For most drivers, this is the best rate environment since 2022.

Your car model matters more than you think.

The Toyota RAV4 and Honda CR-V are the most affordable new cars to insure in 2026, costing about $214 per month for full Coverage — roughly 14% below average. The most expensive is the Tesla Model Y at $354 per month. Markel, if you are shopping for a new car, factor in insurance before you buy.

Age affects your rate — a lot.

Young drivers in their teens and early 20s typically pay two to three times more than drivers in their 40s and 50s. Rates generally peak at age 18 and fall steadily through age 25.

Knowing the national averages is useful. But your real rate depends on your state. That is where the biggest differences hide.

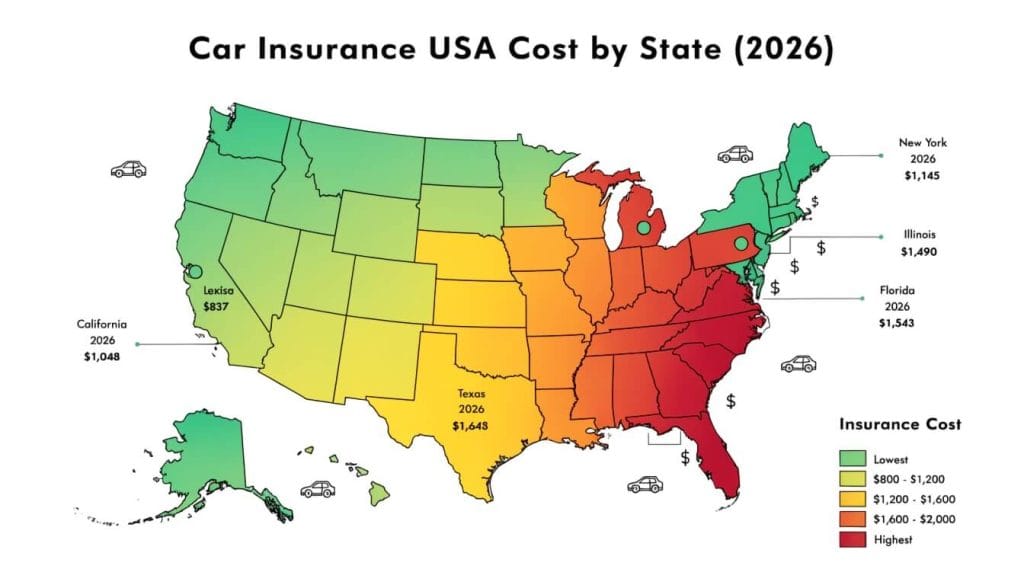

Car Insurance by State — How Much You Actually Pay

Car insurance rates in the USA vary more by state than almost any other financial product. Your ZIP code can change your annual premium by $1,000 or more — sometimes $2,000.

Here is a breakdown of the states most relevant to drivers searching for car insurance today.

Car Insurance in California

California drivers pay an average of $2,133 annually — or $178 per month — for full coverage car insurance, according to Experian data from March 2026. Growfusely, that is below what some other high-cost states charge, but still significantly above the national average.

California’s rates reflect several pressures that compound. A 2025 law doubled California’s minimum liability requirements, raising baseline payouts on every policy and pushing premiums up across all coverage tiers. About 17% of California drivers are uninsured — one of the higher rates nationally. When those drivers cause accidents, insured drivers absorb the cost through higher premiums. Mighty Roar

One key fact California drivers often miss: California law prohibits insurance companies from using your gender or credit history when setting your rate, making it one of only a few states with this protection. WhitePress Your driving record and ZIP code carry more weight here than in almost any other state.

Saving tip for California: Compare at least four quotes — rates in California vary more between insurers than in most states. GEICO offers the lowest rates in 9 of the 10 analyzed California cities. Broworks

Car Insurance in New York and New York City

New York has the highest full Coverage car insurance rates of any state, averaging over $4,000 per year — driven by high repair costs, frequent claims, and expensive medical care. Send

New York City drivers pay even more than the state average. Dense traffic, high theft rates, and the cost of medical care in the metro area all push premiums up. Drivers in upstate New York — in cities like Buffalo or Albany — typically pay 30–40% less than NYC drivers for the same Coverage.

Saving tip for NYC: If you drive fewer than 7,500 miles per year, ask your insurer about a low-mileage discount. Many NYC residents qualify but never ask. [INTERNAL LINK: “How to Lower Car Insurance Rates in New York”]

Car Insurance in Illinois and Chicago

Cheap car insurance in Illinois is easier to find outside of Chicago. Cook County — where Chicago sits — carries some of the state’s highest rates due to dense traffic, higher theft rates, and more frequent accident claims.

Illinois requires a minimum of 25/50/20 — meaning $25,000 per person and $50,000 per accident for bodily injury, plus $20,000 for property damage. That is slightly higher than many states, which adds a floor to minimum coverage costs.

Saving tip for Illinois: Bundle your renters or home insurance with your auto policy. Most major insurers offer 10–15% off both policies when you combine them.

Car Insurance in Texas and Houston

Full coverage car insurance in Texas costs more than in most states — and the gap has grown sharply. Texas had the largest increase in car insurance costs among US states over five years, with rates rising 60.97% between 2020 and 2025. Siege Media [CITE: ValuePenguin 2026]

Texas is an at-fault state — meaning the driver who causes an accident pays for the other party’s damages through their liability coverage. This differs from no-fault states, where each driver’s own insurer covers their injuries regardless of who caused the crash. In at-fault states like Texas, having adequate liability limits matters more.

Cheap car insurance in Houston is available — but only if you compare. Houston’s rates are higher than the Texas state average due to traffic density, storm exposure, and high vehicle theft rates. GEICO, State Farm, and Progressive all compete heavily in Houston, which can work in your favor.

Saving tip for Texas: Ask about a telematics discount — a program where you install a small device or app that tracks your driving habits. Safe drivers in Texas can typically save 10–25% through programs like Progressive’s Snapshot or State Farm’s Drive Safe & Save.

Car Insurance in Los Angeles

Car insurance in Los Angeles ranks as the most expensive city rate in California. On average, drivers in Los Angeles pay $4,201 per year for car insurance — $1,191 above the California state average and $1,688 above the national average. Practical Ecommerce

Los Angeles combines nearly every factor that raises insurance costs: extreme traffic density, one of the country’s highest concentrations of uninsured drivers, high vehicle theft rates, and expensive repair labor. Los Angeles leads California in vehicle theft, with over 208,000 cars stolen statewide in 2023 — roughly twice the number in Texas. Mighty Roar

Saving tip for LA: If your car is older and fully paid off, consider dropping collision coverage. If the car is worth less than $6,000, you may pay more in collision premiums over three years than the car is worth.

Your state sets the floor for what you pay. Your choices set the ceiling. Now let’s look at what those choices actually mean in real life.

Real-World Use Cases — How Car Insurance Works for Different Drivers

Here is where most people get surprised. Car insurance does not work the same way for everyone — and the same policy can produce very different outcomes depending on your situation.

Scenario 1 — The New Driver in Chicago

Priya, 22, just got her first car in Chicago and wanted to save money. She chose minimum Coverage at $97 per month. Three months later, she hit a parked car in a parking lot. The damage to the other car was $4,800. Her liability coverage paid it. Her own car needed $2,100 in repairs. Her policy covered none of it. Priya paid out of pocket. Full Coverage would have added $62 per month — less than her Netflix, Spotify, and gym membership combined.

Scenario 2 — The Smart Shopper in Texas

Derek, 41, had been with the same insurer in Dallas for 9 years. He assumed loyalty meant good rates. When his renewal came in at $2,340 for the year, he spent 20 minutes on a comparison site. He found the same full Coverage from a competitor for $1,740. He switched. He saved $600 that year without changing a single thing about his Coverage. [INTERNAL LINK: “Best Car Insurance Companies in Texas 2026”]

Scenario 3 — The Unexpected Claim in Los Angeles ★

Sandra, 35, drove a 2019 Honda Civic in Los Angeles. She carried full Coverage and paid $196 per month — above average, but reasonable for LA. In January 2026, her car was stolen from outside her apartment. Most people expect this story to end badly. But Sandra’s comprehensive Coverage paid her $18,400 — the actual cash value of her car. She had a new car within two weeks. Without the comprehensive, she would have received nothing. In a city where over 208,000 cars were stolen in one year, comprehensive Coverage is not optional — it is essential.

These three cases show that the “right” Coverage is not about spending the most. It is about aligning your Coverage with your actual risk. That brings us to the mistakes that cost drivers the most money.

Risks and Common Mistakes With Car Insurance in the USA

Most car insurance mistakes do not happen when you file a claim. They happen months or years before, when you first choose your policy and then forget about it.

Mistake 1: Choosing the state minimum and calling it “covered.”

The minimum legal requirement is not the same as adequate protection. In Texas, the minimum property damage limit is $25,000. The average new car costs over $48,000. If you total someone’s new car, you pay the difference out of pocket.

Mistake 2: Never shop at renewal.

Most drivers renew automatically. In 2026, five of the ten largest car insurance companies are expected to lower their rates — meaning your current insurer may no longer offer the best price, even if it did last year. Siege Media Set a 30-day reminder before every renewal date.

Mistake 3: Not telling your insurer about life changes.

Moving to a new ZIP code, adding a teen driver, or changing jobs can all affect your rate — for better or worse. Failing to update your policy can void your Coverage on a claim.

Mistake 4: Skipping uninsured motorist coverage.

This is the mistake most articles never mention. According to the Insurance Information Institute (III), roughly 1 in 8 American drivers has no insurance. SeoProfy: If one of them hits you and has no insurance, your own liability coverage does not protect you. Uninsured motorist coverage — often just $10–$20 extra per month — does. In states like California, Florida, and Michigan, where uninsured driver rates run high, this Coverage is not optional for careful drivers.

Mistake 5: Insuring a low-value car with full Coverage.

If your car is worth $4,000 and you carry a $1,000 deductible on collision, your insurer will only ever pay a maximum of $3,000. You may pay more in premiums over two years than the Coverage is worth. Run the math before you renew.

Pro Tip: Before your next renewal, pull your car’s current market value from Kelley Blue Book. If your car’s value minus your deductible is less than six months of collision premiums, drop the collision coverage. That single adjustment saves many drivers $400–$700 per year — with no meaningful loss of protection.

Advanced Insights — What Most Car Insurance Guides Skip

But here’s the interesting part most guides skip entirely.

1. Your credit score affects your rate in 48 states — silently.

Most drivers do not know that insurers in 48 states use your credit-based insurance score to set your premium. This is not the same as your regular credit score, but it draws from similar data. A driver with poor credit can pay 50–100% more than an identical driver with excellent credit, same age, same car, same driving record. California, Hawaii, Massachusetts, and Michigan prohibit this practice. If you live in one of those four states, you have one less variable working against you.

2. Telematics programs reward behavior, not just history.

Programs like Progressive’s Snapshot, State Farm’s Drive Safe & Save, and Allstate’s Drivewise track how you actually drive — your speed, braking, and time of day. Safe drivers can earn discounts of 10–25%. But there is a catch: if the data shows risky driving, some programs can raise your rate. Read the terms before you sign up.

3. Gap insurance protects you from a hidden financial risk.

If you finance a new car and total it in the first two years, your insurer pays the car’s current market value — not what you owe the bank. A new car loses 20% of its value in the first year. Gap insurance — typically $20–$40 per month — covers the difference between what your car is worth and what you still owe. Most dealers offer it, but your own insurer is usually cheaper.

These three insights separate drivers who manage their insurance well from those who pay the bill and hope for the best.

Frequently Asked Questions About Car Insurance in the USA

Q: How much does car insurance in the USA cost per month in 2026?

A: The average cost of full coverage car insurance in the USA is $208 per month in 2026, according to ValuePenguin data. Minimum Coverage averages $131 per month. Your actual rate depends on your state, age, driving record, and coverage level — so your rate may be higher or lower than the national average.

Q: What is the cheapest state for car insurance in the USA?

A: Vermont, Maine, and New Hampshire typically offer the lowest car insurance rates in the USA. Vermont drivers pay an average of $125 per month for full Coverage — about 40% below the national average. Low population density, fewer accidents, and milder weather all contribute to lower rates in these states.

Q: How do I get cheap car insurance in the USA step by step in 2026?

A: Start by comparing at least three quotes using a comparison tool like The Zebra or NerdWallet. Then check every discount your insurer offers — bundling, safe driver, low mileage, and paying upfront often reduce rates by 10–30%. Review your deductible and drop collision on older low-value cars. Repeat this process every 12 months at renewal.

Q: Is full coverage car insurance worth it in the USA?

A: Full Coverage is typically worth it if your car is worth more than $8,000, if you financed or leased your vehicle, or if you could not afford to replace your car out of pocket. For older cars worth less than $4,000, minimum Coverage or liability-only may save you more than you risk.

Q: What are the biggest mistakes people make with car insurance?

A: The most costly mistakes are choosing the state minimum without understanding what it covers, never shopping at renewal, skipping uninsured motorist coverage, and keeping full Coverage on a low-value car. Any one of these mistakes can cost drivers $500–$7,000 or more over time.

Q: Does my credit score affect my car insurance rate in the USA?

A: Yes — in 48 out of 50 states, insurers use a credit-based insurance score to set your rate. Drivers with poor credit can pay significantly more than drivers with excellent credit for the same Coverage. California, Hawaii, Massachusetts, and Michigan are the only states that prohibit this practice.

Q: How do car insurance rates in California compare to the national average?

A: California drivers pay an average of $178 per month for full Coverage in 2026 — above the national average of $208 per month in some datasets and below in others, depending on the data source. Los Angeles drivers pay considerably more, averaging around $196–$303 per month, depending on the source and coverage level. California bans the use of credit scores and gender in rate-setting, making it unique among most states.

Conclusion

The bottom line about car insurance in the USA is simpler than it looks.

You pay for protection against financial loss. The right policy matches your real risk — not the minimum the law requires, and not the maximum any insurer will sell you. Three things matter most: your coverage level, your deductible, and how often you shop.

Here are the three things to do this week:

Look up your state’s average rate. If you pay significantly more, you have a strong reason to shop around.

Set a renewal reminder. Never auto-renew without comparing at least two other quotes first.

Check for uninsured motorist coverage. If you do not carry it, add it—it typically costs less than $20 per month and protects you from the 1 in 8 uninsured drivers.

Car insurance in the USA does not have to be complicated. It just takes 20 minutes of attention at renewal to make sure you are not overpaying for the protection you already have.

Disclaimer: This article is for informational purposes only and does not constitute financial or insurance advice. Please consult a licensed financial advisor or insurance professional before making any decisions.