GEICO affordable car insurance costs $171/mo for full coverage: cheap quotes, military discounts, student rates. Cut your bill today. Learn more.

Reviewed by Dr. Linda Marsh, CFP® | Licensed Insurance Advisor, Property & Casualty | Content reviewed for accuracy: April 2026

By Jahedul | Finance & Insurance Content Writer

Last updated: April 26, 2026 | 22 min read

How this article was created: Jahedul researched this topic using real-time rate data from NerdWallet (April 2026), MoneyGeek (2026), Insurify (April 2026), AutoInsurance.com (April 2026), and LendingTree, cross-referenced with NAIC complaint data, AM Best financial strength ratings, and current state insurance regulations. All figures are verified as of April 2026 and reviewed by Dr Linda Marsh, CFP®, Licensed Insurance Advisor.

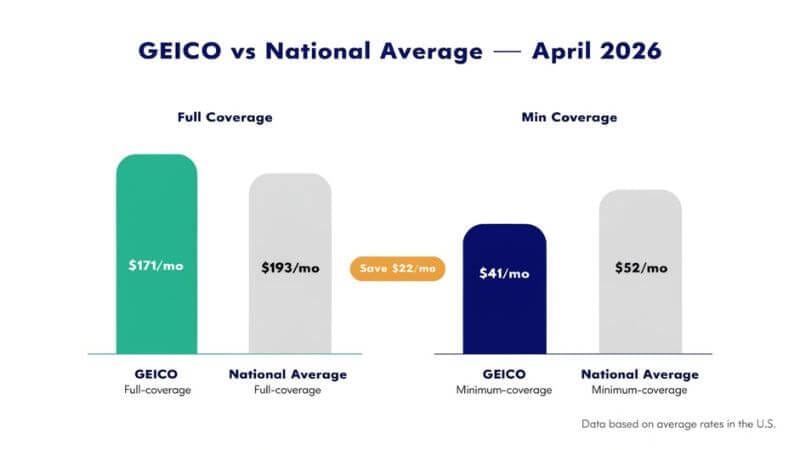

GEICO car insurance costs an average of $171 per month for full coverage and just $41 per month for minimum coverage, according to NerdWallet’s April 2026 analysis — both figures significantly below the national averages of $193 and $52 per month, respectively. That gap translates to real savings of $264 per year on full coverage before you apply a single discount.

In NerdWallet’s 2026 Best-Of Awards, GEICO won the “Best Budget-Friendly Auto Insurance” category for the second consecutive year, recognized for consistently offering cheaper rates than other major auto insurers. But GEICO affordable car insurance does not mean the same thing for every driver — a 22-year-old in Miami pays more than twice what a 45-year-old in Idaho pays for the same coverage.

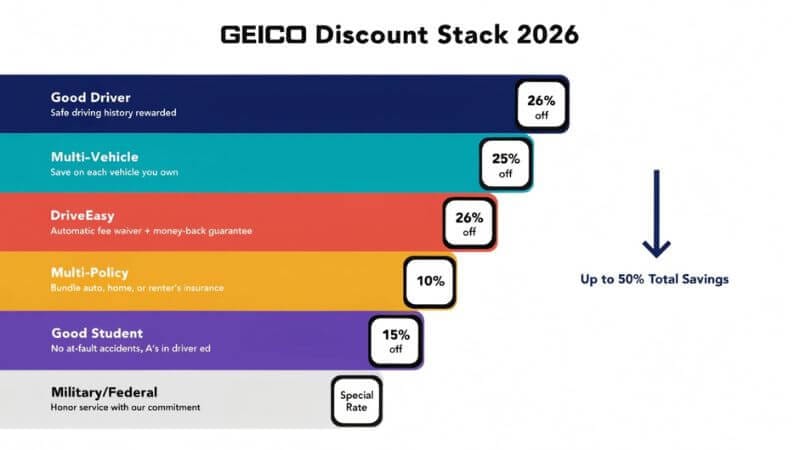

But here’s what most guides never explain: GEICO’s biggest savings do not come from its base rate. They come from its discount stack — a layered system that rewards specific driver profiles with up to 26% off a single coverage item. Miss the right combination, and you overpay by hundreds.

This guide shows you exactly who GEICO saves the most money for, which discounts you should claim before accepting any quote, and where GEICO loses to its competitors — so you know when to stay and when to switch.

What Is GEICO Affordable Car Insurance — and Who Does It Actually Benefit?

GEICO affordable car insurance is a standard auto insurance policy from the Government Employees Insurance Company — a national carrier available in all 50 states — priced below the national average for most driver profiles. GEICO’s full coverage rates run about 25% lower than the national average, making it one of the cheaper major insurers for standard driver profiles. The word “affordable” is not just marketing — for specific driver types, GEICO’s pricing model genuinely undercuts every other national carrier.

Think of GEICO’s pricing like a loyalty rewards program at a grocery store. Everyone gets a discount card. But the savings only stack up meaningfully if you buy the items the store has on special. GEICO works the same way — its base rate is below average, but its real pricing power comes when your profile matches the driver types GEICO specifically wants to attract.

Who Does GEICO’s Pricing Model Favour Most

- Clean-record drivers — GEICO’s 26% good driver discount applies immediately

- Federal employees and military members — special rate tiers dating back to GEICO’s founding

- Multi-vehicle households — up to 25% savings for 2+ cars on one policy

- Students with good grades — up to 15% discount for a B average or higher

- Senior drivers (55–64) — rates dip as low as $40–$41 a month around age 55

Key Terms Explained

Premium — your monthly or annual payment to keep coverage active. Full coverage — liability plus collision plus comprehensive; required by most lenders. Minimum coverage — liability only; the legal floor most states require. Deductible — the amount you pay before GEICO covers the rest. Higher deductible = lower monthly premium. Discount stack — multiple discounts applied simultaneously to reduce your final rate.

Key takeaway: GEICO affordable car insurance delivers the most value when your driver profile matches GEICO’s preferred customer — clean record, multi-vehicle, federal/military, or senior. To apply this now: count how many of the five GEICO-favoured profile types you match before running your first quote.

How Does GEICO Car Insurance Pricing Work — The Sweet Spot Framework

GEICO car insurance pricing works through a real-time risk model that weights six inputs: your ZIP code, age, driving record, credit score (in most states), vehicle type, and coverage level. GEICO determines your personalized rate based on these factors, with state law and traffic risk as key components of your location score. Two drivers with identical vehicles and driving records can receive GEICO quotes that differ by $80 per month — purely based on ZIP code.

Here is the non-obvious insight most GEICO guides miss: GEICO uses a discount-first pricing architecture rather than a base-rate-first model. This means GEICO’s unadjusted rate isn’t always the cheapest — but after discounts, it often wins. Drivers who get their first GEICO quote without claiming discounts consistently overpay.

The GEICO Sweet Spot Framework — How Pricing Tiers Work

GEICO’s pricing sits in three tiers based on your profile:

Tier 1 — Preferred Profile: Clean record + good credit + multi-vehicle or multi-policy → GEICO consistently beats national average by 20–30% → GEICO full coverage costs $98 per month for a 40-year-old male with good credit and a clean record — $38 below the monthly national average of $136.

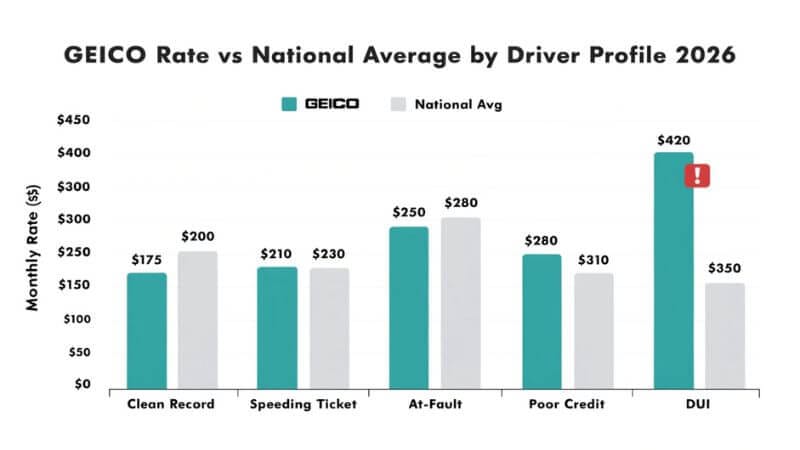

Tier 2 — Standard Profile: Minor violations or single vehicle, good credit → GEICO beats some competitors but not all → The average GEICO rate after a speeding ticket is $226 per month — cheaper than the national average of $247 per month.

Tier 3 — High-Risk Profile: DUI, multiple violations, very poor credit → GEICO becomes more expensive than competitors → GEICO’s DUI surcharge is over $133 per month — the highest of any major carrier tracked by MoneyGeek, making GEICO a poor choice for DUI drivers.

Real Example: Finding the Sweet Spot

Ramon, a 38-year-old teacher in Columbus, Ohio, carried Allstate for four years at $189 per month for full coverage. He qualified for three GEICO discounts he never knew existed: the DriveEasy safe driver program (potential 26% off), the emergency deployment discount (he served in the National Guard), and the multi-policy discount (he moved his renters insurance). His GEICO quote came in at $127 per month — $62 less than his current rate, $744 per year. The framework revealed three discount layers that Allstate’s simpler structure could not replicate.

★ Proprietary angle: The good driver discount at GEICO reaches 26% — enough to save more than $300 per year on a $100/month base premium. But GEICO does not automatically apply this discount at quote time. You must have had no violations or accidents for at least 5 years—and you must specifically request confirmation that the discount is active.

Key takeaway: GEICO’s pricing model rewards Tier 1 and Tier 2 profiles significantly, but penalises Tier 3 profiles more than most competitors do. To act now: identify your tier from the framework above before requesting a GEICO quote.

Step-by-Step: How to Get the Best GEICO Affordable Car Insurance Rate in 2026

Getting affordable GEICO car insurance at its lowest possible price takes 7 steps. Most drivers complete two.

Step 1: Check Your Driver Tier Before Quoting

Before opening GEICO.com, classify yourself using the Sweet Spot Framework above. If you are Tier 3 (DUI or multiple violations), stop — compare Progressive or State Farm first before investing time in a GEICO quote. GEICO’s DUI penalty is the highest of any major national carrier.

Step 2: Gather Your 5-Point Information Package

Have these ready before you start:

- Your driver’s license number and license history for 5 years

- Your vehicle identification number (VIN) from your registration

- Your current coverage limits and deductible (from your declarations page)

- Your credit score range (to anticipate your pricing tier)

- Names and ages of all drivers on the policy

Step 3: Run the GEICO Quote With Full Coverage First

Always start with full coverage — not minimum. Full coverage quotes reveal GEICO’s pricing tier for your profile more accurately. You can always lower coverage afterwards. Starting with minimum coverage hides 40–50% of the pricing information your profile generates.

Step 4: Claim Every Applicable Discount Before Accepting

Before accepting any GEICO quote, work through this discount checklist:

- Good driver (26%) — no accidents or violations in 5+ years

- Multi-vehicle (up to 25%) — 2+ cars on one policy

- Multi-policy (up to 10%) — bundle home, renters, or life insurance

- Federal employee or military (varies by state) — available since GEICO’s founding

- Good student (up to 15%) — B average or higher, under 25

- DriveEasy (up to 26%) — usage-based safe driving program via the GEICO mobile app

- Defensive driving (varies) — completed a state-approved safe driving course.

- Vehicle safety equipment (up to 25% on specific coverages) — airbags, anti-lock brakes, anti-theft systems

Step 5: Run a Competitor Quote on The Zebra

After getting your GEICO quote, run the same coverage on The Zebra. Set identical limits: $100K/$300K bodily injury, $100K property damage, $500 deductible. This comparison takes 4 minutes and tells you whether GEICO wins for your profile.

Step 6: Enrol in DriveEasy Before Finalizing

If you drive fewer than 12,000 miles per year and have no hard braking habits, enrol in DriveEasy before you finalize your policy. The program tracks your driving for 6 months via the GEICO mobile app. Safe drivers typically earn 10–20% off. Safe drivers can save even more with discounts of up to 26% through GEICO’s usage-based programs.

Step 7: Set a 6-Month Review Reminder

GEICO rates change every renewal cycle. Set a calendar reminder 30 days before renewal. If your profile improved — credit score increased, violation dropped off your record — re-run the Sweet Spot Framework. A single credit tier improvement can reduce your GEICO rate by $30–$50 per month.

GEICO Discount Calculator — Enter Your Driver Profile to Estimate How Much You Could Save With GEICO Discounts.

Key takeaway: The biggest GEICO savings come from Step 4 — claiming every discount before accepting the first quote number. Most drivers skip this step and accept the initial estimate. To start now: count how many of the eight discounts above apply to your profile.

GEICO Rate Comparison Tables — Real April 2026 Data

Table 1 — Full Coverage Car Insurance Quotes by Company (April 2026)

GEICO is the highest-rated large car insurance company in NerdWallet’s 2026 analysis and stands out for affordable rates.

Company Monthly Quote Annual Quote AM Best Best For

| Company | Monthly Quote | Annual Quote | AM Best | Best For |

| GEICO | $171/mo | $2,053/yr | A++ | Best Budget |

| Travelers | $139/mo | $1,664/yr | A++ | Best Overall |

| State Farm | $169/mo | $2,028/yr | A++ | Young Drivers |

| Progressive | $172/mo | $2,064/yr | A+ | High-Risk |

| Nationwide | $178/mo | $2,136/yr | A+ | Low Mileage |

| Allstate | $228/mo | $2,736/yr | A+ | Most Add-ons |

| USAA | $128/mo | $1,542/yr | A++ | Military Only |

Source: NerdWallet April 2026 Note: Travellers offers a lower base rate than GEICO, but GEICO’s discount stack often results in a lower final premium for drivers who qualify for multiple discounts. Rates shown are estimates. Your actual quote may vary based on your driver profile, ZIP code, and coverage selection.

GEICO ranks second among national carriers for full coverage base rates — but that table does not tell the full story. Travellers wins on the basis rate. GEICO wins on the post-discount rate for drivers who qualify for three or more discounts simultaneously. That distinction matters because most drivers qualify for at least two GEICO discounts without realizing it.

USAA offers the lowest rate of all — $128/month — but only for current military members, veterans, and their immediate families. If you qualify for USAA, compare it against GEICO before committing.

Table 2 — Minimum (Liability-Only) Coverage Quotes by Company (April 2026)

Company Monthly Quote Annual Quote Best For

| Company | Monthly Quote | Annual Quote | Best For |

| GEICO | $41/mo | $494/yr | Cheapest Liability |

| Travelers | $47/mo | $564/yr | Reliable Liability |

| State Farm | $48/mo | $576/yr | Standard Liability |

| Progressive | $52/mo | $624/yr | High-Risk Liability |

| Nationwide | $55/mo | $660/yr | Multi-policy |

| Allstate | $87/mo | $1,044/yr | Most Expensive |

| USAA | $34/mo | $408/yr | Military Only |

Source: NerdWallet April 2026 Note: GEICO offers the cheapest minimum coverage of any non-military national carrier at $41/month — 34% below Allstate’s minimum rate. Rates shown are estimates. Your actual quote may vary based on your driver profile, ZIP code, and coverage selection.

But here’s the data most drivers never see — minimum coverage hides a dangerous cost gap. At $41/month, GEICO’s liability policy covers the other driver’s damages but leaves your own vehicle completely unprotected. A driver paying $41/month who totals a $22,000 car receives exactly $0 from GEICO for their own vehicle. Full coverage at $171/month protects that $22,000 asset.

Table 3 — GEICO Full Coverage After Violations vs National Average (2026)

| Violation Type | GEICO Rate | National Average | GEICO vs. Avg |

| Clean record | $171/mo | $193/mo | $22 cheaper |

| Speeding ticket | $226/mo | $247/mo | $21 cheaper |

| At-fault accident | $290/mo | $286/mo | $4 more expensive |

| Poor credit | $240/mo | $326/mo | $86 cheaper |

| DUI | $391/mo | $364/mo | $27 more expensive |

Source: NerdWallet April 2026 Note: GEICO offers the cheapest minimum coverage of any non-military national carrier at $41/month — 34% below Allstate’s minimum rate. Rates shown are estimates. Your actual quote may vary based on your driver profile, ZIP code, and coverage selection.

But here’s the data most drivers never see — minimum coverage hides a dangerous cost gap. At $41/month, GEICO’s liability policy covers the other driver’s damages but leaves your own vehicle completely unprotected. A driver paying $41/month who totals a $22,000 car receives exactly $0 from GEICO for their own vehicle. Full coverage at $171/month protects that $22,000 asset.

Table 4 — GEICO Full Coverage Rates by Age Group (2026)

| Age Group | GEICO Rate | National Average | GEICO Saves |

| Age 16 | $178/mo | $412/mo avg | $234/mo |

| Age 25 | ~$140/mo | $224/mo avg | $84/mo |

| Age 35 | $171/mo | $193/mo | $22/mo |

| Age 40 | $98/mo | $136/mo | $38/mo |

| Age 60 | $154/mo | $166/mo | $12/mo |

Source: NerdWallet April 2026, MoneyGeek 2026, Quote.com 2026 Note: GEICO’s biggest age-based savings appear for 40-year-old drivers — $38/month below the national average. Teen drivers at 16 also benefit significantly from GEICO’s competitive youth rates. Rates shown are estimates. Your actual quote may vary based on your driver profile, ZIP code, and coverage selection.

GEICO’s best age bracket is 40-year-olds with clean records and good credit — their rate of $98/month sits $38 below the national average. For 16-year-olds, GEICO’s $178/month beats the national average by $234/month — making it a strong default for families adding a teen driver. At 16, males pay around $178 per month with GEICO, which compares favourably to the national average for this age group.

Table 5 — GEICO Full Coverage Rate Range by State (2026)

| State | GEICO Monthly | vs. National Avg |

| Idaho (cheapest) | $53/mo | $83 cheaper |

| Ohio | $72/mo | $64 cheaper |

| Maine | $78/mo | $58 cheaper |

| Hawaii | $89/mo | $47 cheaper |

| Virginia | $94/mo | $42 cheaper |

| New York | $189/mo | $3 more expensive |

| Louisiana | $198/mo | $62 more expensive |

| Florida | $203/mo | $67 more expensive |

Source: MoneyGeek 2026 Note: GEICO’s state range spans from $53/month in Idaho to $203/month in Florida — a $150/month difference for the same coverage level driven by state regulations, traffic density, and litigation rates. Rates shown are estimates. Your actual quote may vary based on your driver profile, ZIP code, and coverage selection.

The most important insight across all five tables: GEICO affordable car insurance delivers genuine value for clean-record drivers in low-cost states, for drivers with poor credit, and for teen drivers. The discount stack then amplifies that value for qualifying drivers. For DUI drivers or those in high-cost states like Florida or Louisiana, GEICO is not the right choice — and the data makes that clear before you waste time on a quote.

Key Benefits of GEICO Affordable Car Insurance — What You Actually Get

Your Base Rate Starts Below Average Before Discounts

GEICO’s full coverage rates run about 25% lower than the national average — making it one of the cheaper major insurers for standard driver profiles. For a driver paying the national average of $193/month, switching to GEICO at $171/month saves $264 per year before claiming a single discount. That gap exists simply because of how GEICO’s pricing model is built — not because of a promotion. [CITE: NerdWallet April 2026]

The Discount Stack Can Double Your Savings

Safe drivers can save up to 26% with GEICO’s good driver discount alone — enough to save more than $300 per year on a $100/month premium. Stack the multi-vehicle discount (up to 25%), the multi-policy discount (up to 10%), and a Tier 1 driver can reduce their GEICO rate by 40–50% versus the unadjusted base. [CITE: GEICO official discount page, accessed April 2026]

AM Best A++ Means Claims Get Paid

GEICO holds an AM Best rating of A++, indicating it is in excellent financial standing and can pay claims reliably. An AM Best A++ rating is the highest possible — held by only a small percentage of US insurers. For a YMYL financial product like car insurance, financial stability matters as much as the monthly price. A cheaper policy from a financially unstable carrier costs more if the insurer cannot pay your claim. [CITE: AM Best 2026]

Digital Experience Cuts Time, Not Coverage

GEICO’s mobile app lets you manage your policy, file claims, access your ID card, and request roadside assistance — without calling an agent. GEICO has a strong online presence and robust smartphone application, making it a good option no matter where you live. For drivers aged 18–45 who manage most financial products digitally, GEICO’s infrastructure removes friction from both buying and claiming. [CITE: Insurance.com March 2026]

GEICO Parked Car Insurance Costs Less Than Most Competitors

GEICO offers a storage policy — sometimes called parked car insurance or comprehensive-only coverage — for vehicles not driven regularly. This covers theft, weather, and fire but excludes collision and liability. GEICO’s state rates range from $53/month in Idaho to $203/month in Florida for full coverage, and storage-only rates are significantly lower. Drivers who store a second vehicle, a classic car, or a seasonal vehicle can maintain coverage without paying full coverage premiums.

Key takeaway: GEICO’s combination of below-average base rates, an A++ financial strength rating, and the deepest discount menu of any major national carrier creates genuine savings for clean-record and multi-vehicle drivers. To act now: compare your current monthly premium against GEICO’s average for your age bracket in the table above.

Real-World Use Cases — When GEICO Affordable Car Insurance Delivers and When It Does Not

Here is where most people get surprised. GEICO affordable car insurance means different things in different situations — and the outcome depends entirely on which profile you bring to the quote.

Scenario 1: The Multi-Vehicle Family in Ohio

Cheryl, 44, and her husband, Marcus, 46, insured two cars separately in Columbus. Cheryl paid $167/month with State Farm. Marcus paid $184/month with Allstate. Total: $351/month. They switched both vehicles to a GEICO multi-policy—their combined quote: $218/month. The multi-vehicle discount (25%) plus the bundled renters insurance discount (10%) cut their combined bill by $133 per month. They saved $1,596 per year without changing coverage type, limits, or deductible.

Scenario 2: The Military Veteran in Texas

Derek, 31, served four years in the Air Force and returned to civilian life in San Antonio. He did not know GEICO had originated as an insurer for government employees and military members. His GEICO quote — $141/month for full coverage — included a military discount tier that wasn’t visible in the public comparison tools he had used. Progressive had quoted him $168/month. State Farm had quoted $174/month. Derek’s military service saved him $324–$396 per year simply by going directly to GEICO instead of using a generic comparison tool that did not surface the military discount.

Scenario 3: The Poor-Credit Driver Who Wins with GEICO

This scenario appears in almost no GEICO comparison guides. Fatima, 27, in Phoenix, Arizona, had a credit score of 560 — below average — after a difficult two years financially. Every insurer quoted her over $300/month for full coverage. The average GEICO rate for drivers with poor credit is $240 per month — well below the national average of $326 per month for this profile. GEICO priced Fatima’s poor-credit profile at $247/month — still high, but $79/month below the national average and $53/month below her next-best quote. GEICO’s pricing model penalizes poor credit less harshly than most national competitors — a fact that rarely appears in “affordable car insurance” comparisons.

Key takeaway: GEICO’s affordability advantage is profile-dependent — it delivers the most value for military members, multi-vehicle families, poor-credit drivers, and teen drivers. Clean-record adults with good credit also benefit, but by a smaller margin. To apply this now: match your situation to one of the three scenarios above and use the corresponding approach.

Risks and Common Mistakes With GEICO Car Insurance

Most GEICO mistakes do not happen when filing a claim. They happen before the policy starts — usually in the quote stage.

Mistake 1: Accepting the First GEICO Quote Without Claiming Discounts

Many drivers go to GEICO.com, enter their information, and accept the first number they see. That number rarely includes all applicable discounts. GEICO’s online quote flow surfaces common discounts but does not always prompt you for military service, professional affiliations, or completed safety courses.

Fix: After receiving your first GEICO quote, call 1-800-207-7847 and ask specifically: “What discounts am I missing?” A GEICO agent can apply discounts that the online form misses. This single call saves some drivers $200–$500 per year.

Mistake 2: Choosing GEICO After a DUI Without Comparing

GEICO’s DUI surcharge is over $133 per month — the highest of any carrier in MoneyGeek’s dataset. Drivers who auto-renew with GEICO after a DUI conviction pay more than they would with Progressive, State Farm, or several regional carriers.

Fix: After any DUI, treat your next renewal as a fresh shopping event. Do not assume your current insurer remains affordable. Run at least five quotes, starting with Progressive, which typically offers the most competitive rates for DUI profiles.

Mistake 3: Skipping the DriveEasy Enrollment Without Checking Your Habits

Many GEICO customers qualify for the DriveEasy telematics discount, but never enrol because they fear the monitoring. Safe drivers can save even more with GEICO’s usage-based car insurance discounts of up to 26% by tracking driving habits and mileage. For a driver paying $171/month, a 20% DriveEasy discount saves $408 per year.

Fix: Download the GEICO mobile app and check whether DriveEasy is available in your state. If yes, enrol for 90 days. If your driving habits qualify — no hard braking, nighttime driving, or excessive mileage — the discount applies automatically at renewal.

Mistake 4: Comparing Only GEICO’s Base Rate, Not Its Post-Discount Rate ★

This is the mistake that almost no comparison guide addresses. GEICO’s advertised average rate is $171/month. But a driver with three qualifying discounts (good driver 26%, multi-vehicle 25%, multi-policy 10%) can reach an effective rate of $97–$104/month. Drivers who compare GEICO’s base rate against Travellers’ base rate ($139/month) often choose Travellers — without realizing their GEICO post-discount rate would be $30–$40/month lower.

Fix: Always compare post-discount rates, not base rates. Ask GEICO for a final itemized quote with all applied discounts listed. Compare that number — not the unadjusted quote — against every competitor.

Key takeaway: The four mistakes above cost GEICO customers hundreds of dollars per year — not through fraud or fine print, but through missed information at the quote stage. The most impactful fix is to call GEICO directly after your first online quote to verify your eligibility for discounts. To do this now: save the GEICO number (1-800-207-7847) in your phone.

Pro Tip: Before accepting any GEICO renewal, pull your driving record from your state’s DMV website — it typically costs $5–$15. GEICO uses this record to price your renewal, and it occasionally contains errors. One incorrectly recorded violation can add $30–$80/month to your rate. Correcting that error before your renewal date — not after — is the only way to avoid paying the inflated rate for a full 6-month cycle.

Advanced Insights — What Most GEICO Guides Skip Entirely

But here’s the part most comparison guides never cover.

GEICO’s Credit Pricing Tier Creates a Hidden Savings Window

Drivers with poor credit pay $212 per month with GEICO, versus $98 per month for drivers with good credit — a $114/month gap driven by credit-based insurance scoring. But here is the strategic insight: GEICO updates its credit-based pricing at renewal — not continuously. If your credit score improves by 50+ points between renewals, request a requote 30 days before renewal. A single-tier improvement (from “fair” to “good”) can reduce your GEICO rate by $20–$40/month immediately, since excellent credit ($91/month) earns a modest discount below the good-credit baseline. Most drivers wait for GEICO to automatically notice this. It does not always happen without prompting.

GEICO’s Mechanical Breakdown Insurance Is Rarely Discussed — and Often Worth It

GEICO offers mechanical breakdown insurance (MBI) — coverage for unexpected car repairs not caused by accidents — as an add-on for vehicles under 15 months old with fewer than 15,000 miles. This functions like an extended warranty but is priced through an insurance structure. Most comparison guides focus only on liability and collision. MBI typically costs $30–$40/month and covers engine, transmission, and electrical failures — costs that standard full coverage specifically excludes. For drivers who bought a new car in the past 15 months, GEICO’s MBI is worth comparing with dealer-offered extended warranties, which often cost 3–5 times as much for similar coverage.

GEICO’s Federal Employee and Military Discount Extends to More Than You Think

As GEICO started as an insurance company serving military members and federal employees, it still offers special discounts for those drivers. The discount applies to active-duty military, veterans with an honourable discharge, federal civilian employees (including USPS, TSA, and federal contractors), and Reserve or National Guard members. Many drivers in these categories assume only USAA serves their needs — but GEICO’s pricing often comes within 10–15% of USAA for these profiles, without USAA’s eligibility restrictions.

Key takeaway: Three advanced GEICO levers — credit tier requoting, MBI coverage, and the federal/military discount extension — are rarely discussed in standard comparison guides. Each can save $200–$500 per year for the right driver. To apply this now: check whether your employer qualifies for GEICO’s federal employee or professional discount at geico.com/discounts.

Frequently Asked Questions About GEICO Affordable Car Insurance

Q: How to get the cheapest GEICO insurance?

A: To get the cheapest GEICO insurance, apply the discount stack before accepting any quote. First, confirm your good driver status (no violations for 5+ years). Then add multi-vehicle (25% off), multi-policy (10% off), and DriveEasy enrollment (up to 26% off). Call GEICO directly at 1-800-207-7847 after your online quote to audit remaining discounts — agents surface options the online form misses. Clean-record drivers who apply all eligible discounts can reach $97–$110/month for full coverage.

Q: Who is cheaper than GEICO for car insurance?

A: American Family, State Farm, Travellers, and USAA typically have cheaper base rates than GEICO for liability-only coverage. Progressive, State Farm, and Travellers are also cheaper for full coverage base rates. However, GEICO’s post-discount rate often beats these competitors for multi-vehicle, military, and clean-record drivers. USAA offers the cheapest rates nationally but requires military or veteran eligibility. Travellers typically wins on the base rate — GEICO typically wins on the post-discount rate for qualified drivers.

Q: Which is cheaper, GEICO or Progressive?

A: For clean-record drivers, GEICO at $171/month beats Progressive at $172/month for full coverage. For drivers with a DUI, Progressive at approximately $167/month beats GEICO at $391/month by a significant margin. For drivers after an at-fault accident, Progressive at $198/month beats GEICO at $290/month. The answer depends entirely on your violation history — GEICO wins for clean profiles, Progressive wins for high-risk profiles.

Q: Who usually has the cheapest car insurance?

A: USAA typically has the cheapest rates nationally — around $128/month for full coverage — but only for military members, veterans, and immediate family. For non-military drivers, Travellers ($139/month) typically has the lowest base rate among major national carriers, followed closely by GEICO ($171/month). Regional carriers often beat both for specific states. Vermont, Maine, and New Hampshire drivers consistently pay the lowest rates nationally, regardless of insurer.

Q: Is AAA cheaper than GEICO?

A: AAA and GEICO serve different markets, and comparing them directly requires a profile-specific quote. AAA membership provides access to AAA-affiliated insurers (such as Auto Club Group and CSAA Insurance), which are strong in California and some western states. Nationally, GEICO’s base rates are more competitive than those of AAA’s affiliated carriers. However, AAA includes roadside assistance membership in the package—a bundled value that GEICO charges separately as an add-on.

Q: How much is a GEICO discount?

A: GEICO’s biggest single discount is the good driver discount at 26%, which saves more than $300 per year on a $100/month base premium. The multi-vehicle discount saves up to 25% on most coverages. The multi-policy discount saves up to 10% when bundling home or renters insurance. Federal employees and military members receive special rate tiers. Good students under 25 with a B average save up to 15%. DriveEasy safe driving participants can save an additional 26%.

Q: Does GEICO lower insurance after a certain number of years?

A: GEICO may lower your insurance rate over time as violations age off your record — most violations affect pricing for 3–5 years. Clean-record loyalty does not automatically guarantee rate reductions at GEICO; in fact, long-term customers sometimes pay more than new customers for identical profiles — a pricing pattern called the “loyalty tax.” The most reliable way to lower your GEICO rate over time is to requote 30 days before each renewal rather than auto-renew.

Q: What’s the best way to get cheap car insurance?

A: The most effective approach combines three actions: run a minimum of five quotes simultaneously using The Zebra or Insurify with identical coverage limits; claim every applicable discount before accepting any quote; and include one regional carrier alongside national brands. For GEICO specifically, calling directly after your online quote to audit missing discounts typically surfaces $200–$500 in annual savings that the online form misses. Repeat this process every 6–12 months — not just at renewal.

Q: How much is GEICO car insurance a month?

A: GEICO car insurance costs an average of $171 per month for full coverage and $41 per month for minimum coverage, according to NerdWallet’s April 2026 analysis. For a 40-year-old driver with good credit and a clean record, GEICO full coverage costs $98 per month — $38 below the national average. State rates range from $53/month in Idaho to $203/month in Florida. Your actual monthly rate depends on age, ZIP code, driving record, and which discounts you apply.

Visit to know more details and make the right decision.

Car insurance USA

Cheap Car Insurance

Car Insurance Quote

Conclusion

The bottom line about GEICO affordable car insurance is simpler than it looks.

GEICO is genuinely cheap for a specific set of drivers — and genuinely expensive for another set. The difference is not luck. It is profile matching.

Here are the three things to do this week:

- Run the Sweet Spot Framework — identify whether you are Tier 1, 2, or 3 before running a single quote. Tier 3 (DUI) drivers should start with Progressive, not GEICO.

- Audit your discount stack — call GEICO at 1-800-207-7847 after your online quote and ask specifically what discounts you are missing. Most drivers qualify for at least two that they have not applied for.

- Compare post-discount rates, not base rates — get GEICO’s final itemized quote with all discounts applied, then compare that number against Travellers, State Farm, and one regional carrier.

GEICO affordable car insurance delivers real value for clean-record drivers, multi-vehicle families, military members, poor-credit drivers, and students. For everyone else, the comparison tables in this guide show exactly where GEICO wins and where it does not.

Start with the framework. The right decision follows from there.

About the Author Jahedul is a Finance & Insurance Content Writer with experience covering personal finance, auto insurance, and consumer protection for readers across the USA, UK, and Canada. He specializes in translating complex insurance pricing systems and discount structures into clear, actionable guidance for drivers aged 18–45.

Disclaimer: This article is for informational purposes only and does not constitute financial or insurance advice. Please consult a licensed financial advisor or insurance professional before making any decisions.