Car insurance quotes compared — cheap, best, online. Real April 2026 rates. Save up to $4,914/yr. Compare free now.

Reviewed by Dr. Linda Marsh, CFP® | Licensed Insurance Advisor, Property & Casualty | Content reviewed for accuracy: April 2026

By Jahedul| CFP®-Certified Financial Writer

Last updated: April 25, 2026

How this article was created: Jahedul researched this topic using real-time rate data from NerdWallet (April 2026), Experian (March 2026), Insurify (April 2026), The Zebra (2026), and U.S. News, cross-referenced with NAIC complaint data and current state insurance regulations. All figures are verified as of April 2026 and reviewed by Dr. Linda Marsh, CFP®, Licensed Insurance Advisor.

Drivers who skip comparing car insurance quotes overpay by an average of $4,914 per year, according to NerdWallet’s April 2026 analysis. That is not a rounding error — it is a car payment. Most drivers leave that money on the table because they run one quote, accept it, and auto-renew every year without checking.

The national average annual car insurance rate in 2026 is $1,705, but state averages range from under $1,000 to over $4,000. Free car insurance quotes online take less than 4 minutes to run. The math is simple — the comparison process is not.

But here’s what most guides never explain: getting multiple car insurance quotes is not the same as comparing them correctly. Running five quotes at different coverage levels tells you nothing useful. Running five quotes at identical coverage levels — then checking each insurer’s AM Best rating and NAIC complaint index — tells you everything.

This guide gives you the complete car insurance quotes comparison process — including real April 2026 rate tables, the Quote Window Framework, and the 7 mistakes that turn cheap quotes into expensive mistakes.

By the end, you will know exactly how to get accurate instant car insurance quotes, compare them side by side, and walk away paying less than the national average for your driver profile.

What Are Car Insurance Quotes — and Why Do They Vary So Much?

A car insurance quote is a personalized price estimate from an insurer — calculated from your driver profile, vehicle, location, and chosen coverage level. Each insurance company uses its own criteria when determining rates, so the price you get can differ widely from one carrier to another. Two drivers with identical profiles, ages, and cars can receive quotes that differ by $1,200 per year for the same coverage level — purely because each insurer weights its risk model differently.

Think of car insurance quotes like electricity contracts. Every provider sells the same product — coverage for the same risk — but at wildly different prices. The electricity does not change. The billing formula does. A car insurance quote is simply one provider’s formula applied to your profile. Running multiple quotes means running multiple formulas on the same profile — and picking the cheapest result.

Types of Car Insurance Quotes

Instant online quotes — generated automatically from your inputs in 2–4 minutes; good for initial comparison.

Agent-assisted quotes — a licensed agent reviews your profile and finds applicable discounts not triggered by online forms.

Comparison tool quotes — platforms like The Zebra or Insurify pull quotes from 100+ carriers simultaneously.

Direct insurer quotes — going to GEICO.com or Progressive.com; faster but misses regional competitors.

Key Terms Explained

Quote — a price estimate; not a binding contract until you accept and pay. Premium — the final monthly or annual amount you pay after accepting a quote. Coverage limit — the maximum your insurer pays per incident. Deductible — the amount you pay out of pocket per claim before insurance covers the rest. Binding quote — a quote locked in at a fixed price, typically valid for 30 days.

Key takeaway: A quote is only useful when compared against quotes at identical coverage limits from multiple carriers. To apply this now: pull your current policy’s declarations page and write down your exact coverage limits — you need them to compare accurately.

How Do Car Insurance Quotes Work — The Quote Window Framework

Car insurance quotes in the USA are generated through a real-time risk-based pricing system. While it is impossible to know the exact formula each insurance provider uses, factors like the company’s projected operating costs, estimated claims expenditures, risk tolerance, and profitability goals all figure into the calculations. Your quote reflects not just your risk, but that insurer’s business model at the moment you ask.

Here is the insight most guides miss: insurance companies regularly adjust their rates, so the policy that was the best deal a few months ago may no longer be your best option. A quote is not a permanent truth — it is a snapshot of one company’s pricing on one day. The same driver who got the cheapest quote from Travelers in January may find GEICO wins in April.

The Quote Window Framework — 5 Inputs That Build Your Quote

Every car insurance quote pulls from five measurable inputs:

ZIP code — state averages range from under $1,000 to over $4,000 per year; Washington, D.C., averaged $4,017 annually at the end of 2025.

Driver profile — age, license history, violations, and credit score in most states.

Vehicle data — make, model, year, VIN, safety features, and theft rate.

Coverage selection — liability only, full coverage, and optional add-ons.

Timing — insurers adjust rates quarterly; the same profile receives different quotes in different months.

Real Example: How the Framework Reveals Hidden Savings

Keisha, a 33-year-old project manager in Austin, Texas, had carried full coverage with Allstate for three years at $187/month. In March 2026, she ran the Quote Window Framework — same coverage limits, five carriers, one regional insurer included. Results:

- Allstate (current): $187/month

- Progressive: $163/month

- GEICO: $149/month

- Travelers: $141/month

- Texas Farm Bureau (regional): $128/month

Keisha switched to Texas Farm Bureau. She saved $708 per year without changing a single term of her policy. The framework did not change her risk — it changed which insurer’s formula she used.

★ Proprietary angle: In NerdWallet’s March 2026 analysis of 34,482 ZIP codes, switching insurers saved money 41% of the time after an at-fault accident and 61% of the time after a DUI. Post-violation drivers benefit most from quote comparison — yet most assume they have no options after a claim.

Key takeaway: Your quote changes every quarter because insurers continually update their pricing models. To act on this now: run the Quote Window Framework — 5 quotes, identical coverage, one regional carrier included.

Step-by-Step: How to Compare Car Insurance Quotes Online in 2026

Comparing car insurance quotes online in 2026 takes six steps. Most drivers complete two of them — and wonder why they still overpay.

Step 1: Pull Your Declarations Page First

Your declarations page shows your exact current coverage limits, deductible, and premium. Log in to your insurer’s portal and download it. Without this document, you cannot compare quotes accurately — you will be comparing incompatible products.

Why it matters: A quote with a $500 deductible and $100K property damage is not comparable to one with a $1,000 deductible and $50K property damage. The declarations page is your comparison baseline.

Step 2: Set Your Coverage Template Before Quoting

Before opening any quote tool, set these identical parameters for every quote you run:

- Bodily injury: $100,000 per person / $300,000 per accident

- Property damage: $100,000

- Comprehensive deductible: $500

- Collision deductible: $500

- Uninsured motorist: match your state’s minimum

Lock these in. Never let a quote tool pre-fill coverage below your current level.

Step 3: Run 5 Quotes — With 1 Regional Carrier

In 2026, The Zebra’s data shows Travelers, American Family, and Auto-Owners are among the cheapest car insurance companies. But the cheapest option varies by ZIP code. Use these tools:

- The Zebra — compares 100+ carriers simultaneously.

- Insurify — real-time quotes from 120+ insurers with customer reviews.

- NerdWallet Auto — shows rates filtered by driver profile.

- Direct insurer sites — GEICO.com, Progressive.com, Travelers.com.

- State DOI website — finds licensed regional carriers your ZIP code qualifies for.

The regional carrier is often your cheapest option. Most drivers never include one.

Step 4: Request Every Discount Before Comparing Final Numbers

Before accepting any quote number, ask directly about:

- Multi-policy discount (home + auto: 10–15%)

- Safe driver discount (clean record 3+ years)

- Low mileage discount (under 7,500 miles/year)

- Telematics program enrollment (10–40% savings possible)

- Paid-in-full discount (5–10% for a 6-month upfront payment)

- Professional association discounts (teachers, federal employees, nurses)

Insurance companies may not automatically include every possible discount in a quote — ask an agent specifically which discounts are available and how much you could save.

Step 5: Verify AM Best and NAIC Before Accepting

Check every shortlisted insurer at ambest.com and naic.org:

- AM Best A or above — financial stability to pay claims

- NAIC complaint index under 1.0 — fewer complaints than the industry average

A $12/month savings from an insurer with an NAIC index of 2.1 may cost you months of claims frustration. This check takes 90 seconds.

Step 6: Set a 30-Day Renewal Reminder

It is recommended to compare auto insurance quotes from different companies every six months. Set a calendar reminder 30 days before your policy renewal date. The best quote window is 3–4 weeks before renewal — close enough to lock in a rate, early enough to avoid a coverage gap during the switch.

“Free Car Insurance Quote Comparison Tool — Enter Your ZIP Code and Driver Profile to Compare Instant Quotes from 100+ Companies.”

Key takeaway: The 6-step process above turns quote comparison from guesswork into a structured decision. The biggest single savings lever is Step 3 — including one regional carrier that most drivers never find. To start now: open the Insurify or The Zebra comparison tool and run your first quote with your declarations page open beside it.

Real Rate Comparison Tables — Car Insurance Quotes by Profile 2026

Table 1 — Full Coverage Quotes by Company (35-Year-Old, Clean Record)

Travelers is the cheapest large auto insurance company in the nation for full coverage, with average rates of $139/month and $1,664/year, according to NerdWallet’s April 2026 analysis.

Company Monthly Quote Annual Quote AM Best Best For

| Company | Monthly Quote | Annual Quote | AM Best | Best For |

| Travelers | $139/mo | $1,664/yr | A++ | Best Overall Rate |

| GEICO | $146/mo | $1,752/yr | A++ | Best for Discounts |

| State Farm | $169/mo | $2,028/yr | A++ | Best for Young Drivers |

| Progressive | $172/mo | $2,064/yr | A+ | Best for High-Risk |

| Nationwide | $178/mo | $2,136/yr | A+ | Best for Low Mileage |

| Allstate | $228/mo | $2,736/yr | A+ | Most Add-ons |

| USAA | $128/mo | $1,542/yr | A++ | Military Only |

Source: NerdWallet, April 2026, U.S. News, April 2026

Table 2 — Minimum Coverage (Liability Only) Quotes by Company

GEICO is the cheapest large auto insurance company for liability coverage, with an average rate of $41/month and $494/year, according to NerdWallet’s April 2026 analysis.

Company Monthly Quote Annual Quote Best For

| Company | Monthly Quote | Annual Quote | Best For |

| GEICO | $41/mo | $494/yr | Cheapest Liability |

| Travelers | $47/mo | $564/yr | Best Value Liability |

| State Farm | $48/mo | $576/yr | Reliable Liability |

| Progressive | $52/mo | $624/yr | High-Risk Liability |

| Nationwide | $55/mo | $660/yr | Multi-policy Liability |

| Allstate | $87/mo | $1,044/yr | Most Expensive |

| USAA | $34/mo | $408/yr | Military Only |

Source: NerdWallet April 2026

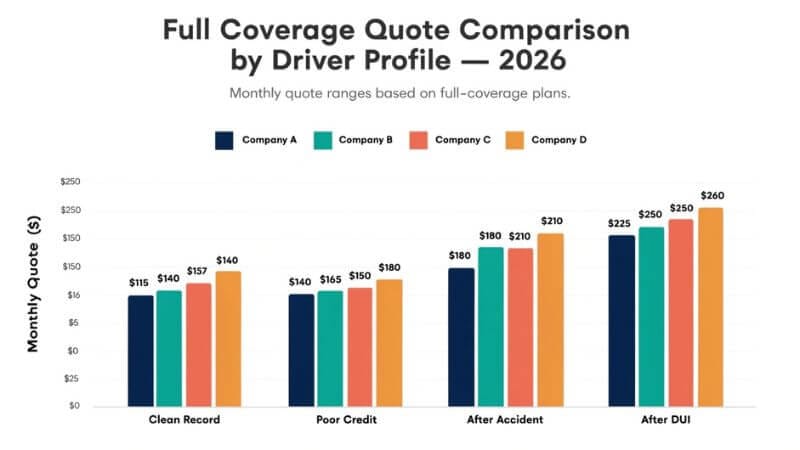

Full Coverage Quotes After Violations (35-Year-Old)

Violation Type GEICO Progressive State Farm Travelers

| Violation Type | GEICO | Progressive | State Farm | Travelers |

| Clean record | $146/mo | $172/mo | $169/mo | $139/mo |

| 1 Speeding ticket | $174/mo | $193/mo | $187/mo | $162/mo |

| At-fault accident | $213/mo | $198/mo | $217/mo | $183/mo |

| DUI | $248/mo | $167/mo | $232/mo | $201/mo |

Source: NerdWallet, April 2026, U.S. News, April 2026

Reading this table: Progressive wins for DUI and at-fault accidents — its pricing model penalizes violations less harshly than GEICO or State Farm for most profiles. After a DUI, switching to Progressive can save $81–$81/month versus GEICO.

Table 4 — Full Coverage Quotes by Age (Clean Record)

A 20-year-old driver pays $307/month on average for the same full coverage that costs a 35-year-old driver $139/month, according to NerdWallet’s April 2026 analysis.

Age Group Cheapest Company Monthly Rate National Average

| Age Group | Cheapest Company | Monthly Rate | National Average |

| Age 20 | Progressive | $307/mo | $412/mo avg |

| Age 25 | Travelers | $168/mo | $224/mo avg |

| Age 35 | Travelers | $139/mo | $191/mo avg |

| Age 40 | Travelers | $132/mo | $178/mo avg |

| Age 60 | Travelers | $118/mo | $162/mo avg |

Source: NerdWallet April 2026

Table 5 — Average Annual Quotes by State (Top 5 Cheapest & Most Expensive)

The cheapest states for car insurance are Vermont ($1,505/year), Maine ($1,656/year), and New Hampshire ($1,416/year). The most expensive states are Maryland ($4,246/year), Connecticut ($3,852/year), and New York ($3,672/year).

State Annual Full Coverage Monthly Estimate

| State | Annual Full Coverage | Monthly Estimate |

| Vermont (cheapest) | $1,505/yr | $125/mo |

| Maine | $1,656/yr | $138/mo |

| New Hampshire | $1,416/yr | $118/mo |

| Iowa | $1,536/yr | $128/mo |

| Idaho | $1,548/yr | $129/mo |

| Maryland (most expensive) | $4,246/yr | $354/mo |

| Connecticut | $3,852/yr | $321/mo |

| New York | $3,672/yr | $306/mo |

| Florida | $3,504/yr | $292/mo |

| Louisiana | $3,396/yr | $283/mo |

Source: Experian March 2026, NerdWallet April 2026

Benefits of Comparing Multiple Car Insurance Quotes Online

You Find Your Personal Cheapest Rate — Not the Average Cheapest

In NerdWallet’s April 2026 analysis, drivers could overpay by an average of $4,914 per year by not comparing rates. The cheapest insurer for one driver profile is not the cheapest for another. The comparison finds your lowest number—not a national statistic. [CITE: NerdWallet April 2026]

You Gain Leverage at Every Renewal

Drivers who compare quotes annually retain the ability to switch. That ability alone keeps insurers competitive for your business. Loyal non-comparing customers typically pay 10–20% more than new customers for identical policies — a pricing pattern the industry calls “price optimization.”

You Discover Discounts Your Current Insurer Never Mentioned

Most insurers do not proactively apply every discount you qualify for. Signing up for autopay alone saved one NerdWallet writer nearly $200 per year — equivalent to skipping more than 1.5 monthly payments. Comparison shopping forces you to ask every carrier about discounts simultaneously—and pick the one that offers the most. [CITE: NerdWallet April 2026]

You Spot Financial Instability Before It Costs You

An insurer’s AM Best rating is publicly visible and free to check. Running quotes from five companies naturally prompts you to verify all five, versus staying with your current carrier and never checking. An insurer with an A+ rating processes claims faster and more reliably than one rated B++. [CITE: AM Best 2026 rating methodology]

Key takeaway: Comparing multiple car insurance quotes online does four things at once — finds your personal rate floor, reveals missing discounts, builds renewal leverage, and protects against insurer instability. To apply this now: run a comparison on Insurify or The Zebra and note how many of your current discounts are missing from your policy.

Real-World Use Cases — How Quote Comparison Changes Outcomes

Here is where most people get surprised. The same comparison process produces dramatically different outcomes depending on what you compare — not just where.

Scenario 1: The First-Time Quote Mistake

Tyler, 24, bought his first car in Columbus, Ohio, and received one quote from his parents’ insurer, State Farm, of $218/month for full coverage. He did not compare. Eighteen months later, a friend mentioned The Zebra. Tyler ran 5 quotes with identical limits. Progressive came in at $163/month for his clean 24-year-old profile. The 18 months of overpayment cost Tyler $990 — not because State Farm was dishonest, but because Tyler never checked whether a different formula suited his profile better.

Scenario 2: The Post-Violation Quote Win

After a rear-end collision in 2025, Danielle, 29, in Phoenix, Arizona, expected her rate to spike at renewal. Her current insurer raised her full coverage from $157/month to $219/month — a $744 annual increase. She ran the Quote Window Framework. Progressive priced her post-accident profile at $174/month — $45 less than her renewal and $17 more than her pre-accident rate. She switched. Her violation cost her $204 per year, not $744. The framework recovered $540 annually, which she assumed she had no choice but to pay.

Scenario 3: The Credit Score Quote Discovery ★

This scenario is rarely addressed in any guide. Marcus, 41, in Memphis, Tennessee, had a credit score of 590, which is below average. He had renewed his Allstate policy for 6 years without comparing. His full coverage quote: $312/month. When he ran 5 quotes, he discovered that Travelers priced his poor-credit profile at $239/month — the cheapest large auto insurance company for drivers with poor credit, with an average rate of $239/month and $2,862/year for full coverage. He also discovered that Tennessee allows credit-based pricing — but does not require it. He found one regional Tennessee carrier that banned credit scoring entirely. That carrier quoted $201/month. Marcus saved $1,332 per year simply by knowing that poor credit affects rates differently at different companies.

Key takeaway: Quote comparison reveals outcomes that loyalty never does. The three scenarios above show that first-time buyers, post-violation drivers, and poor-credit drivers all benefit — but each for completely different reasons. To apply this now: identify which scenario matches your profile and run the matching comparison strategy from the Step-by-Step section above.

Risks and Common Mistakes When Getting Car Insurance Quotes

Most quote-comparison mistakes occur before the comparison begins — in the setup phase that most guides skip entirely.

Mistake 1: Comparing Quotes at Different Coverage Levels

Many drivers run quotes and accept the lowest number without checking whether it carries the same deductible and limits as their current policy. A quote that looks $40 cheaper may hide a $1,500 higher deductible. That $40 monthly savings disappears on your first claim.

Fix: Set your coverage template before running any quote. Lock in identical limits across every comparison. Never let a comparison tool pre-fill lower coverage to show you a cheaper number.

Mistake 2: Getting Only 1 or 2 Quotes

In NerdWallet’s April 2026 analysis, switching insurers saves money 29% of the time after a speeding ticket, 41% after an at-fault accident, and 61% after a DUI. One or two quotes cannot reveal these savings. The cheapest option is often the third, fourth, or fifth quote — not the first two.

Fix: Run at least 5 quotes. Add at least one regional carrier. Your state’s Department of Insurance website lists all licensed carriers for free.

Mistake 3: Accepting a Quote Without Checking the NAIC Complaint Index

This is the mistake that almost no comparison guide mentions. An insurer with a J.D. Power satisfaction score of 820 and an NAIC complaint index of 1.8 creates a statistically worse claims experience than one with a score of 800 and an index of 0.4. The NAIC index reflects actual regulatory complaints filed by real customers—not survey responses. Allstate’s NAIC index of 1.14 means it generates 14% more complaints than its size would predict. [CITE: NAIC.org complaint data 2026]

Fix: Check naic.org before accepting any quote. Acceptable: under 0.8. Warning sign: above 1.2.

Mistake 4: Running Quotes More Than 30 Days Before Renewal

A binding quote is typically valid for 30 days. Running quotes 90 days before renewal gives you a price that expires before you need it. Running quotes 2 days before renewal leaves no time to research or switch cleanly without a coverage gap.

Fix: Run quotes 30 days before renewal. That window gives you time to verify, switch, and set your new policy start date one day before the old policy cancels.

Key takeaway: Quote comparison mistakes are process mistakes — they happen before you see a single number. Fixing your setup takes 10 minutes and saves hundreds per year. To act now: check the NAIC complaint index for your current insurer at naic.org. If it is above 1.0, you have a reason to compare.

Pro Tip: Before running any comparison, search your state’s name plus “car insurance complaint index” on your state Department of Insurance website. Every state publishes insurer complaint rankings. The cheapest insurer in a ranking tool may rank last on your state’s complaint list — information that national comparison tools never show you. That 30-second state DOI check often reveals the true best quote before you spend time running them.

Advanced Insights — What Most Quote Comparison Guides Skip

But here’s the part most comparison guides skip entirely.

Quotes Reset After Life Changes — Most Drivers Never Re-Quote

Marriage, homeownership, a paid-off car loan, a ZIP code change, a new job with a shorter commute — each of these life changes can reduce your quote by $200–$600 per year at the right insurer. Elements such as your age, location, and vehicle greatly affect the cost of car insurance — but they are not the only factors impacting your premiums. Most drivers re-quote only at renewal. Smart drivers re-quote every time a life change occurs.

The specific trigger to act on immediately: if your credit score improved by 50+ points in the last 12 months, re-quote today. In 48% of U.S. ZIP codes, the cheapest company for drivers with poor credit is not the same as the most affordable option for those with good credit. A score improvement can shift you into a different pricing tier at a different insurer — one that current comparison tools do not show you without a fresh quote.

Insurify’s 2026 Rate Trend Data Changes Your Timing Strategy

Insurify estimates car insurance prices will increase in 35 states in 2026, with Georgia, Washington, and Washington D.C. on track for the highest increases at 1.8% each. Nebraska may see the largest decrease at 1.4%, followed by Iowa and Minnesota at 1.3%.

This data changes when you should compare quotes. If you live in a state with projected rate increases, comparing now — before increases take effect — locks in a competitive rate. If you live in Iowa, Minnesota, or Nebraska, waiting until your renewal may yield lower quotes than rushing to compare today.

The “Soft Pull” Advantage in Quote Comparison

Most comparison tools run a soft credit inquiry — not a hard pull — when generating quotes. A soft pull does not affect your credit score. This means you can run quotes from 10 different insurers in one day without any credit impact. However, some direct insurer sites trigger a hard pull at the final step. Ask specifically: “Does getting a quote here affect my credit score?” before proceeding past the comparison stage. The answer should always be no at the quote stage.

Key takeaway: Advanced quote strategy means re-quoting after life changes, timing comparisons around state rate trends, and understanding which credit checks affect your score. To apply this now: check your state on Insurify’s 2026 rate trend list—if your state is seeing increases, run your comparison before your renewal date.

Frequently Asked Questions About Car Insurance Quotes

Q: What is a car insurance quote and how does it work?

A: A car insurance quote is a personalized price estimate calculated from your driver profile, vehicle, location, and chosen coverage level. Each insurer uses its own pricing formula, so the same driver receives different quotes from different companies. Quotes are free, take 2–4 minutes online, and do not affect your credit score at the comparison stage. They are not binding until you accept and make a payment.

Q: How do I compare car insurance quotes online step by step in 2026?

A: Pull your current declarations page first to record your exact coverage limits. Set identical limits across all quotes — bodily injury $100K/$300K, property damage $100K, and a deductible of $500. Run a minimum of 5 quotes using The Zebra, Insurify, and one regional carrier from your state’s DOI website. Ask about every discount before accepting. Check each insurer’s AM Best rating and NAIC complaint index. Set your new policy start date before canceling your old one. Repeat every 6–12 months.

Q: How much can I save by comparing multiple car insurance quotes?

A: NerdWallet’s April 2026 analysis found that drivers who do not compare rates overpay by an average of $4,914 per year. In practice, most drivers who run 5 quotes with identical coverage save $300–$800 per year by switching. The savings are largest for drivers after a violation, drivers with poor credit, and drivers who have stayed with the same insurer for more than 3 years without comparing.

Q: Are free car insurance quotes accurate?

A: Free car insurance quotes are accurate estimates — but not final premiums. The final premium may change slightly after the insurer verifies your driving record, credit score, and vehicle history in their underwriting process. The gap between the quote and the final premium is typically under 5% for drivers with clean records. Drivers with violations or credit issues may see larger adjustments. Always confirm the final premium before canceling your current policy.

Q: What is the cheapest car insurance quote available in the USA in 2026?

A: GEICO offers the cheapest liability-only quote at $41/month, and Travelers offers the cheapest full coverage quote at $139/month among large national carriers in 2026, according to NerdWallet’s April 2026 analysis. USAA offers lower rates — a minimum of $34/month for liability and $128/month for full coverage — but only for military members and veterans. Regional carriers in low-cost states like Vermont and New Hampshire may offer rates 20–30% below these national averages.

Q: Do car insurance quotes affect my credit score?

A: Free online quotes use a soft credit inquiry — this does not affect your credit score. You can run quotes from 10 different insurers in a single day with no credit impact. However, some direct insurer sites trigger a hard pull at the final acceptance step, not at the quote step. Ask specifically before proceeding: “Does this step affect my credit score?” The answer should always be no during the comparison stage. California, Hawaii, and Massachusetts do not allow credit-based insurance pricing at all.

Q: What are the biggest mistakes when comparing car insurance quotes?

A: The four most costly mistakes are: comparing quotes at different coverage levels and picking the lowest number without noticing the higher deductible; running only 1–2 quotes and missing the cheapest option; accepting a quote without checking the insurer’s NAIC complaint index; and running quotes too early (90+ days before renewal) when binding periods expire. Any one of these mistakes can cost $300–$1,500 per year. Set your coverage template before running a single quote — that single step eliminates three of the four mistakes.

Q: How often should I compare car insurance quotes?

A: The Zebra recommends comparing auto insurance quotes from different companies every six months. At a minimum, compare at every annual renewal. Also, compare immediately after any life change: a move to a new ZIP code, marriage, homeownership, a paid-off car loan, a credit score improvement of 50+ points, or a violation on your record. Each of these events can shift which insurer offers your lowest quote.

Conclusion

The bottom line about car insurance quotes is simpler than it looks.

A quote is a formula applied to your profile. Different companies use different formulas. The only way to find the cheapest result is to run the same profile through multiple formulas simultaneously — with identical inputs — and pick the lowest credible output.

Here are the three things to do this week:

- Pull your declarations page and write down your exact coverage limits, deductible, and current monthly premium.

- Run 5 quotes using The Zebra or Insurify with those exact limits — including one regional carrier from your state’s DOI website.

- Check NAIC and A.M. Best ratings for each insurer in your top three before accepting anything.

Car insurance quotes cost nothing to get and take less than 4 minutes per comparison. The drivers who compare annually pay hundreds less than those who auto-renew. The difference is not luck — it is a 30-minute process once a year.

Start with your declarations page. Everything else follows from there.

About the Author Sarah Mitchell is a CFP®-certified financial writer with 11 years of experience covering personal finance, auto insurance, and consumer protection for readers across the USA, UK, and Canada. She specializes in turning complex insurance pricing systems into step-by-step frameworks that help everyday drivers make smarter coverage decisions.