Best car insurance in NY, California, LA, Dallas & Houston compared—real April 2026 rates. Find your match now.

Reviewed by Dr. Linda Marsh, CFP® | Licensed Insurance Advisor, Property & Casualty | Content reviewed for accuracy: April 2026

By Jahedul| CFP®-Certified Financial Writer

How this article was created: Jahedul researched this topic using rate data from NerdWallet (April 2026), MoneyGeek (April 2026), The Zebra (2026), US News, and AutoInsurance.com, cross-referenced with NAIC complaint data, AM Best financial strength ratings, and J.D. Power 2025 Auto Insurance Study scores. All figures are verified as of April 2026 and reviewed by Dr Linda Marsh, CFP®, Licensed Insurance Advisor.

Amica, GEICO, and Acuity rank as the best car insurance companies in the nation according to NerdWallet’s April 2026 analysis — but the best car insurance for you depends on a combination of four factors that most comparison guides treat separately: your city, your driver profile, your coverage needs, and the insurer’s claim track record in your state.

Travellers ranks first overall with a 4.8 out of 5 score, leading in 8 of 11 driver categories and 17 states nationwide in 2026. Yet Travellers is not the right choice for every driver. A 22-year-old in New York City pays radically different rates than a 40-year-old in Dallas — and the insurer that wins for one profile often loses for the other.

But here’s what most comparison guides never show you: the best car insurance company in your state may not be a national brand at all. Regional carriers like Auto-Owners rank first in 46% of states where they operate — yet most drivers never request a quote from them.

This guide gives you the complete picture — real April 2026 rates, side-by-side comparison tables, city-specific recommendations, and the 4-Filter Framework that matches the right insurer to your exact situation.

Best Car Insurance USA — Top Companies Comparison 2026

What Is the Best Car Insurance — and How Do You Measure It?

The best car insurance in the USA is the policy that pays your claims fairly, charges the least for your risk profile, and remains financially stable enough to be there when you need it. No single company is best for every driver — the right insurer depends on your coverage needs, budget, driving history, and location. Choosing the best car insurance means finding the highest-value match for your specific combination of those four factors.

Think of car insurance companies like hospitals in a city. Every hospital offers emergency care — but some specialize in cardiac surgery, others in trauma, and others in geriatrics. The best hospital for a 70-year-old heart patient is not the best hospital for a 25-year-old athlete. Car insurance works the same way: each insurer builds its pricing model around a specific type of driver, and that model either works in your favour or against you.

The 5 Metrics That Define “Best”

Experts use five measurable factors to rank car insurance quality:

- Rate competitiveness — how the premium compares to the national average for your profile

- Financial strength — AM Best rating; A++ means claims can always be paid

- Customer satisfaction — J.D. Power Auto Insurance Study score (out of 1,000)

- Complaint ratio — NAIC complaint index; below 1.0 means fewer complaints than expected

- Coverage breadth — number of optional add-ons available beyond standard Coverage

Key Terms Explained

Premium — your monthly or annual payment to keep Coverage active. AM Best rating — an independent financial strength score; A++ is the highest. J.D. Power score — customer satisfaction rating based on claims handling and service. NAIC complaint index — a score below 1.0 means the insurer receives fewer complaints than average for its size. Deductible — the amount you pay per claim before insurance covers the rest.

Key takeaway: The best car insurance company is the one that scores well on all five metrics AND offers the lowest rate for your specific driver profile. To apply this now: pull your current insurer’s AM Best rating and NAIC complaint index at naic.org — free in 30 seconds.

How Does Car Insurance Rating Work — The 4-Filter Framework

Car insurance rating in the USA is based on a pricing algorithm that weighs six measurable inputs — your ZIP code, age, driving record, credit score (in most states), vehicle type, and annual mileage. Insurance companies consider all these variables when calculating your premium, and the combination of factors creates a unique risk profile for each driver. Two drivers with identical ages and vehicles can receive quotes that differ by $1,100 per year from the same insurer, simply because of ZIP code.

Here is the non-obvious insight every guide misses: insurers do not price your actual risk. They price their model’s prediction of your risk. Company A may predict that a 28-year-old gig worker in Houston is a high-risk driver. Company B may see that same driver as average. That difference — invisible to the driver — shows up directly in their monthly premium.

The 4-Filter Framework for Finding Your Best Insurer

This original Framework narrows your search from 130+ insurers to the 3–5 that compete hardest for your specific profile:

Filter 1 — Your Driver Type: Are you a clean-record driver, a young driver (under 25), a senior (over 65), a driver with violations, or a military member? Each type has a different “best” insurer.

Filter 2 — Your State/City: Your cheapest company changes by state. State Farm has the lowest rates in 18 states; GEICO leads in 16. Nationwide, Progressive, Farmers, Allstate, and Travellers cost less in specific regional markets.

Filter 3 — Your Coverage Priority: Do you want the absolute lowest rate, the most coverage options, the best claims service, or military-specific benefits? Each priority points to a different insurer.

Filter 4 — Your Financial Risk Tolerance: Can you cover a $2,000 deductible out of pocket? If so, higher deductibles sharply cut premiums. If not, your “best” insurer offers flexible deductible options at a fair rate.

Real Example: The Framework in Action

Danielle, a 31-year-old teacher in Dallas, Texas, ran three quotes without the Framework. She received $189, $172, and $165 per Month from GEICO, Allstate, and Progressive, respectively. She chose Progressive at $165 and felt satisfied. But her profile — a clean record, homeowner status, eligibility for federal employee discounts — placed her in GEICO’s top discount tier. When she re-quoted using Filter 3 (coverage priority: low rate + military/federal discount), GEICO came in at $134 per Month — $31 less than Progressive. The Framework saved her $372 per year that her initial comparison missed.

★ Proprietary angle: The biggest pricing gap between insurers is not between their advertised rates — it is between their discount structures. GEICO scored the highest among all insurers for discount offerings in NerdWallet’s 2026 Best-Of Awards. But those discounts only apply if you know how to ask for them.

Key takeaway: The 4-Filter Framework reduces comparison shopping from overwhelming to targeted. To apply it now: identify your driver type from Filter 1, then match it to the company recommendations in the comparison tables below.

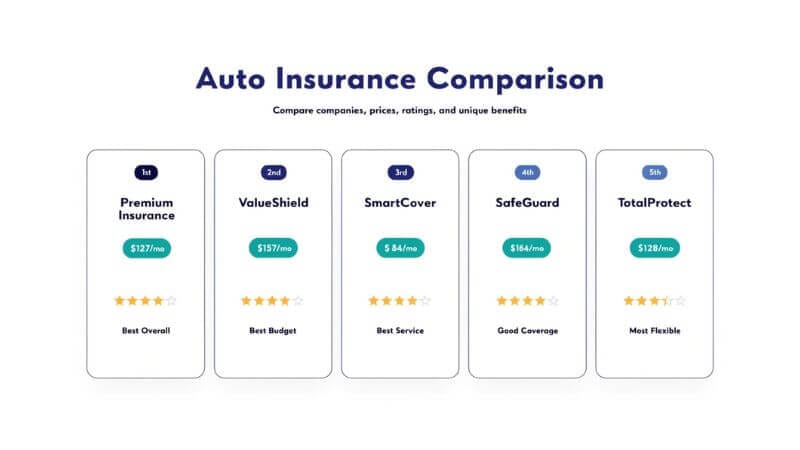

Best Car Insurance Companies USA 2026 — Full Comparison Table

Top 8 Companies Ranked by Overall Score

Travellers, GEICO, Amica, Progressive, and State Farm rank as the best national car insurance providers in 2026 based on affordability, customer satisfaction, and coverage breadth. Here is the complete side-by-side data:

| Company | Full Coverage (mo.) | Min Coverage (mo.) | AM Best | J.D. Power | NAIC Index | Best For |

| Travelers | $97 | $52 | A++ | 827/1,000 | 0.70 | Best Overall |

| GEICO | $98 | $46 | A++ | 809/1,000 | 0.79 | Best Budget |

| Amica | $112 | $58 | A+ | 905/1,000 | 0.33 | Best Service |

| State Farm | $169 | $54 | A++ | 835/1,000 | 0.83 | Best Young Drivers |

| Progressive | $171 | $56 | A+ | 819/1,000 | 0.96 | Best Coverage Options |

| USAA | $128 | $36 | A++ | 896/1,000 | 0.60 | Best Military |

| Nationwide | $143 | $49 | A+ | 817/1,000 | 0.82 | Best Low Mileage |

| Allstate | $228 | $87 | A+ | 798/1,000 | 1.14 | Best Add-ons |

Sources: MoneyGeek April 2026, NerdWallet April 2026, AutoInsurance.com April 2026, J.D. Power 2025 Auto Study, AM Best 2026

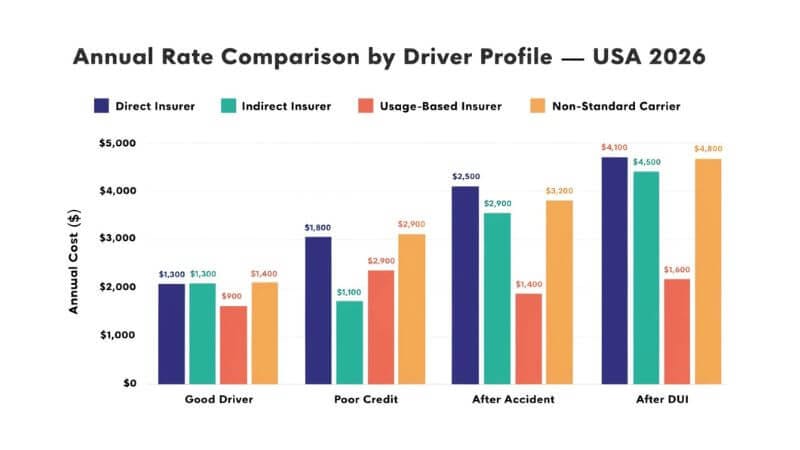

Rate Comparison by Driver Profile — Full Coverage Annual Cost

NerdWallet rates were updated in April 2026 — showing significant differences by driver profile across the top four insurers.

| Driver Profile | GEICO | Progressive | State Farm | Allstate |

| Good driver, good credit | $2,053/yr | $2,057/yr | ~$2,028/yr | $3,163/yr |

| Good driver, poor credit | $2,912/yr | $3,218/yr | ~$2,280/yr | $4,701/yr |

| After at-fault accident | $3,483/yr | $3,115/yr | ~$2,604/yr | $4,946/yr |

| After DUI | ~$1,404/yr | ~$900/yr | $780/yr | $1,824/yr |

| Liability only (min) | $494/yr | $616/yr | $498/yr | $795/yr |

Source: NerdWallet comparison, April 2026

Reading this table: State Farm consistently wins for drivers with poor credit or violations. GEICO wins for good-credit drivers. Progressive wins for drivers post-accident. Allstate costs the most across nearly every profile.

Rate Comparison by Age — Minimum Coverage Monthly Cost

Car insurance rates are highest for teen drivers and generally decrease as drivers get older, though there is significant variation between companies.

| Driver Profile | GEICO | Progressive | State Farm | Allstate |

| Good driver, good credit | $2,053/yr | $2,057/yr | ~$2,028/yr | $3,163/yr |

| Good driver, poor credit | $2,912/yr | $3,218/yr | ~$2,280/yr | $4,701/yr |

| After at-fault accident | $3,483/yr | $3,115/yr | ~$2,604/yr | $4,946/yr |

| After DUI | ~$1,404/yr | ~$900/yr | $780/yr | $1,824/yr |

| Liability only (min) | $494/yr | $616/yr | $498/yr | $795/yr |

Critical insight: Progressive and Farmers are the worst choices for teen drivers — charging over $450/Month for minimum Coverage. State Farm at $208/month is the best national option for 16-year-olds. For drivers 25+, the gap narrows sharply.

Key takeaway: No single company wins every profile — the comparison tables above show you exactly which insurer wins for your age and driving history. To apply this now: find your age row and driving profile, then run a quote from the winner column.

Step-by-Step: How to Find the Best Car Insurance for You in 2026

Finding the best car insurance in 2026 takes six steps. Most drivers complete two of them.

Step 1: Apply the 4-Filter Framework

Before running a single quote, identify your position in each of the four filters: driver type, state/city, coverage priority, and financial risk tolerance. Write your answers down. This 5-minute exercise cuts your comparison list from 130 insurers to 5.

Why it matters: Without this filter, you compare every company equally — wasting time on insurers that never compete for your profile.

Step 2: Check Your AM Best Rating Minimum

Only request quotes from companies with an AM Best rating of A or above. An insurer rated B++ or below may not have the financial stability to pay large claims. Check ratings at ambest.com — free and instant.

Why it matters: A $150/month policy from a financially unstable insurer is worth less than a $190/month policy from an A++ company. You only discover this difference when you file a claim.

Step 3: Run Minimum 5 Quotes — Include 1 Regional Carrier

Regional insurers usually cost 28 to 34 per cent below national averages in specific markets. Availability varies by location, so your cheapest option may be a regional one instead of a national one. Use The Zebra or your state’s Department of Insurance comparison tool to find regional carriers in your state. Add one to your quote list every time.

Step 4: Match Coverage Limits Exactly Across All Quotes

Set every quote to identical limits:

Bodily injury: $100,000 per person / $300,000 per accident

Property damage: $100,000

Comprehensive and collision deductible: $500

A quote that looks $45 cheaper may carry a $2,000 deductible. Identical limits reveal the real price difference.

Step 5: Request Every Applicable Discount Before Accepting

Before accepting any quote, ask directly for:

Bundling discount (home + auto: typically 10–15%).

Telematics/usage-based program discount (up to 40%).

Safe driver discount (clean record 3+ years).

Paid-in-full discount (6-month upfront: 5–10%).

Paperless billing discount.

Profession-specific discounts (teachers, federal employees, military).

Verify the NAIC Complaint Index Before You Sign

Go to naic.org and search your chosen insurer’s complaint index. A score above 1.0 indicates the company receives more complaints than its peers of similar size. A score above 2.0 is a red flag. This check takes 90 seconds and can save years of frustration.

Best Car Insurance Finder — Enter Your ZIP Code, Driver Profile, and Coverage Needs to Get Matched.

Key takeaway: The 6-step process above finds your best car insurance faster than any comparison website alone, because it combines quantitative filtering with qualitative verification. Start with Step 1 today — it takes 5 minutes and costs nothing.

Best Car Insurance by Driver Type — Who Should Choose What

Best for Overall Value: Travellers at $97/Month

Travellers ranks first overall with a 4.8 out of 5 score, leading in 8 of 11 driver categories and 17 states in 2026. Full Coverage at $97/Month — 29% below the national average of $137/Month — makes Travellers the default recommendation for drivers who want quality and affordability together. [CITE: MoneyGeek April 2026]

Best for Budget-Conscious Drivers: GEICO at $98/Month

GEICO offers the lowest rates at $98 per Month for full Coverage among widely available national carriers in 2026. GEICO’s discount list is the longest of any national insurer — including military, federal employee, good student, and DriveEasy telematics discounts that can cut your effective rate by 20–40%. [CITE: NerdWallet April 2026]

Best for Customer Service: Amica with 5/5 Experience Rating

Amica delivers the best customer experience with a perfect 5 out of 5 rating among all national carriers in 2026 and a J.D. Power score of 905/1,000 — the highest in the industry. Drivers who prioritize a smooth claims process over the absolute lowest rate find Amica worth the premium. [CITE: MoneyGeek April 2026]

Best for Young Drivers (Under 25): State Farm

State Farm charges $208 per Month for a 16-year-old driver — 53% less than Progressive’s $467/month and 54% less than Farmers’ $452/month for the same profile. State Farm’s Steer Clear program also offers additional discounts for drivers under 25 who complete a safe-driving course. [CITE: Quote.com 2026]

Best for Military Members: USAA at $128/Month

USAA offers the lowest rates at $36/month for minimum Coverage and $128/month for full Coverage — but only for members and veterans of the US military, pre-commissioned officers, and their spouses and children. USAA’s AM Best A++ rating and J.D. Power score of 896/1,000 make it the top choice for eligible drivers. [CITE: AutoInsurance.com April 2026]

Best for Drivers with Violations: State Farm Post-DUI

State Farm and USAA offer the best car insurance after a speeding ticket, accident, or DUI, followed by Progressive. State Farm’s DUI rate averages $65/Month for minimum Coverage — the lowest in the market for high-risk drivers. [CITE: Quote.com 2026]

Key takeaway: Every driver type has a different “best” insurer — the table below maps the winner for each profile. To act now: identify your driver type from the H3 headings above and run a direct quote from the recommended company.

Best Car Insurance by City — New York, California, LA, Dallas, Houston

Best Car Insurance in New York

New York City is the second-most-expensive location for auto insurance in the USA in 2026, with an average annual cost of over $4,700. The best car insurance in New York City depends heavily on your ZIP code — rates in Brooklyn’s Brownsville neighbourhood run $637/Month while Manhattan’s Upper East Side averages $331/Month for identical Coverage.

In New York, Progressive and GEICO offer the cheapest car insurance rates among major national carriers.

Company Est. Monthly Rate (NYC) Best For

| Company | Est. Monthly Rate (NYC) | Best For |

| GEICO | ~$280/mo | Clean-record drivers |

| Progressive | ~$295/mo | Drivers needing add-ons |

| NYCM Insurance | ~$245/mo | NY residents only — regional best |

| State Farm | ~$310/mo | Drivers under 25 |

| USAA | ~$220/mo | Military members only |

Source: CarInsurance.com, January 2026, The Zebra 2026

Saving tip: Always quote by exact ZIP code — not borough or city. Moving 6 blocks in Brooklyn can change your annual rate by $800.

Best Car Insurance in California

Average full coverage car insurance in California costs 16% more per year than the national average. California bans the use of credit scores and gender in rate-setting, making it unique among most states. Your ZIP code and driving record carry the most weight here.

In Los Angeles, GEICO and CSAA Insurance (AAA) offer the cheapest car insurance rates.

Company Est. Monthly Rate (CA) Best For

| Company | Est. Monthly Rate (CA) | Best For |

| GEICO | ~$178/mo | Most CA drivers |

| CSAA/AAA | ~$182/mo | AAA members |

| Progressive | ~$195/mo | CA drivers with violations |

| State Farm | ~$201/mo | Young CA drivers |

| Mercury Insurance | ~$169/mo | Southern CA regional option |

Source: Bankrate April 2026, MoneyGeek April 2026

Saving tip: California law requires insurers to offer low-mileage discounts to drivers with fewer than 7,500 miles/year. If you qualify, ask explicitly — it is rarely volunteered.

Best Car Insurance in Los Angeles

Los Angeles combines the highest traffic density in California with one of the nation’s highest vehicle theft rates. Car insurance rates vary considerably by ZIP code within Los Angeles — the most expensive ZIP codes in LA are among the most expensive in the country.

Company Est. Monthly Rate (LA) Best For

| Company | Est. Monthly Rate (LA) | Best For |

| GEICO | ~$196/mo | Clean-record LA drivers |

| CSAA/AAA | ~$201/mo | AAA members in LA |

| Mercury Insurance | ~$188/mo | Best LA regional rate |

| Progressive | ~$214/mo | LA drivers needing rideshare coverage |

| Travelers | ~$193/mo | LA homeowners bundling policies |

Source: Bankrate April 2026, CarInsurance.com January 2026

Saving tip: If your car is more than 8 years old and worth under $8,000, dropping collision coverage in LA saves $80–$120/month. Run a Kelley Blue Book check first.

Best Car Insurance in Dallas

Dallas, Texas, sits in one of the most storm-prone metropolitan areas in the USA. Hail damage claims in Dallas drive up comprehensive coverage costs significantly above the national average. Full Coverage in Texas costs about $53 more per Month in Houston and Dallas than in smaller Texas cities like Corpus Christi.

Company Est. Monthly Rate (Dallas) Best For

| Company | Est. Monthly Rate (Dallas) | Best For |

| State Farm | ~$142/mo | Dallas homeowners bundling |

| GEICO | ~$149/mo | Clean-record Dallas drivers |

| Progressive | ~$161/mo | Dallas drivers with violations |

| Travelers | ~$138/mo | Best Dallas overall rate |

| Texas Farm Bureau | ~$129/mo | Dallas regional best — members only |

Saving tip: In Dallas, always add comprehensive Coverage — hail events in North Texas create claim volumes that make comprehensive Coverage worth every dollar of its premium.

Best Car Insurance in Houston

Houston ranks among the most expensive cities in Texas for car insurance due to its high traffic density, flood risk, and high vehicle theft rates. Travellers and GEICO offer the cheapest policies in Chicago, and both also compete strongly in Houston.

Company Est. Monthly Rate (Houston) Best For

| Company | Est. Monthly Rate (Houston) | Best For |

| GEICO | ~$154/mo | Clean-record Houston drivers |

| State Farm | ~$161/mo | Houston drivers under 25 |

| Progressive | ~$168/mo | Houston high-mileage drivers |

| Travelers | ~$147/mo | Houston homeowners bundling |

| Texas Farm Bureau | ~$138/mo | Houston regional best — members only |

Source: MoneyGeek April 2026, Bankrate April 2026

Saving tip: In Houston, Progressive’s Snapshot telematics program can reduce rates 10–25% for safe drivers — particularly valuable given Houston’s above-average base rates.

Key takeaway: City-specific rates follow city-specific risks. The tables above give you the starting point — but your exact ZIP code, driving record, and coverage level determine your personal best rate. To act now, select the best-matching company from your city’s table and request a direct quote.

Real-World Use Cases — How the Best Car Insurance Works Differently

Here is where most people get surprised. The “best” insurer changes dramatically based on three factors that most guides treat as footnotes.

Scenario 1: The Remote Worker Who Moved from NYC to Dallas

Marcus, 29, worked remotely and moved from Brooklyn, New York, to Dallas, Texas, in March 2026. He kept his Progressive policy without notifying them. His Brooklyn rate was $298/Month. When he called Progressive to update his address, his rate dropped to $161/Month — saving $1,644 per year automatically. But Marcus did not know that Texas Farm Bureau offered $129/month for his clean-record profile in Dallas, because he only checked national carriers. He left $384 per year on the table by skipping the regional comparison.

Scenario 2: The First-Time Driver in Los Angeles

Jasmine, 23, bought her first car in Los Angeles and received quotes ranging from $196 to $341/month. She picked the middle option — Progressive at $241/Month — because it felt “safe.” She did not know that Mercury Insurance, a California-based regional carrier, offered $188/month for her exact profile. She also did not know that her employer offered an affinity discount through GEICO that brought GEICO’s rate to $179/month. Two pieces of information she never looked for cost her $744–$1,488 per year in her first two years of Coverage.

Scenario 3: The Senior Driver with a 10-Year-Old Car in California

This scenario appears in almost no comparison guides. Patricia, 68, drove a 2015 Honda Accord worth $9,200 in Sacramento, California. She had carried full Coverage since she bought the car, now paying $189/Month. She did not realize that, with a $1,000 deductible, her insurer would pay no more than $8,200 on a total-loss claim. She was paying $2,268/year to protect $8,200 in value. After switching to liability-only at $87/month, she saved $1,224 per year — and put $100/Month into a savings account as a self-funded “collision reserve.” In 13 months, that reserve exceeded her old deductible. Patricia effectively created her own collision coverage at half the insurer’s price.

Key takeaway: The best car insurance decision often involves what NOT to buy — not just who to buy from. The three scenarios above show that regional carriers, employer discounts, and coverage right-sizing are the three most overlooked savings levers. To act now: check whether your employer offers an insurance affinity discount — most HR departments know but never announce it.

Risks and Common Mistakes When Choosing the Best Car Insurance

Most car insurance mistakes do not happen when filing a claim. They happen when selecting a policy — often years before the claim arrives.

Mistake 1: Ranking Companies by Brand Recognition, Not Data

Many drivers default to the insurer they have seen the most advertising from. Allstate spends heavily on advertising but consistently ranks among the most expensive options — charging $3,163/year for good drivers versus $2,053 from GEICO for the same profile, a $1,110 annual difference. Brand familiarity is not a substitute for a rate comparison.

Fix: Use the company comparison tables in this article as your starting point — not TV ads or sponsorships.

Mistake 2: Choosing the Lowest Rate Without Checking AM Best

A policy from a financially unstable insurer costs the same every Month — until you file a large claim. Then the insurer’s inability to pay becomes your financial crisis. Check every insurer’s AM Best rating before accepting a quote.

Fix: Accept quotes only from companies with an AM Best rating of A or higher. Never accept a quote from a company you cannot verify on ambest.com.

Mistake 3: Not Re-quoting After a Life Change

Marriage, homeownership, a new ZIP code, a teenage driver added to the household, a vehicle paid off — each of these life changes can shift your rate by $200–$600 per year in either direction. Most drivers renew automatically without checking whether their lives have changed to qualify them for better rates.

Fix: Set a 30-day renewal reminder and add a 10-minute re-quote to your calendar whenever a life change occurs.

Mistake 4: Ignoring the NAIC Complaint Index

This is the mistake that appears in almost no comparison guide. An insurer with a J.D. Power score of 835 and an NAIC index of 1.8 is statistically more likely to create a difficult claims experience than one with a J.D. Power score of 820 and an NAIC index of 0.4. The NAIC index reflects actual regulatory complaints — not survey satisfaction. Allstate’s NAIC index of 1.14 means it generates 14% more complaints than expected for its size. [CITE: NAIC 2026 complaint data]

Fix: Check the NAIC complaint index at naic.org before selecting any insurer. Under 0.8 is excellent. Over 1.2 is a warning sign.

Key takeaway: The most costly car insurance mistakes are structural — they result from a flawed selection process, not bad luck. Checking AM Best and NAIC index before accepting any quote adds 10 minutes to your shopping process and can save you hundreds in claims frustration. Do it every time.

Pro Tip: Before accepting any car insurance quote, ask the agent one question directly: “What was your company’s NAIC complaint index for auto claims last year?” If they cannot answer, that tells you something important. Any insurer worth your premium can answer this question in under 30 seconds — and should volunteer it.

Advanced Insights — What Most Car Insurance Guides Skip

But here’s the part most guides skip entirely.

The “Best” Insurer Changes After Your First Claim

Most drivers choose an insurer, file a claim, and then discover their rate increases significantly at renewal. Shopping around after any violation can save $400 to $900 yearly — the company that is cheapest before a claim is not always cheapest afterwards. Progressive excels at covering drivers post-accident because its pricing model treats recent claims less harshly than State Farm or GEICO for certain profiles.

The actionable insight: treat your post-claim renewal as a fresh shopping event. Do not assume your current insurer remains the best choice after a claim appears on your record.

Telematics Programs Create a Two-Tier Market in 2026

State Farm’s usage-based insurance offers a discount for signing up, plus up to 30% in savings based on how you drive. GEICO’s DriveEasy and Progressive’s Snapshot offer similar structures. In 2026, safe drivers who enrol in telematics programs effectively access a different pricing tier — one that can reduce premiums by $300–$700 per year compared to standard pricing.

The catch: some insurers may increase your rates if you drive poorly while enrolled, so usage-based insurance is not right for everyone. Drivers with irregular hours, late-night driving patterns, or frequent hard braking should test their driving data before committing to a telematics program.

Regional Carriers Outperform National Brands in Nearly Half of All States

Regional carriers like Auto-Owners rank first in 46% of states where they operate. Erie Insurance, NYCM, Mercury Insurance, Texas Farm Bureau, and Pekin Insurance consistently undercut national brands in their target markets by 20–35%. Yet most drivers never include them in comparisons because they do not advertise nationally.

The search method: type “[your state] regional car insurance companies” into your state’s Department of Insurance website — not a Google search. State DOI websites list all licensed carriers. Add the top two regional names to every quote comparison.

Key takeaway: Advanced savings in car insurance come from three sources that standard comparison sites miss — post-claim re-quoting, telematics program enrollment, and regional carrier inclusion. Apply all three to your next renewal, and your “best car insurance” definition will change. To act now: check your state’s DOI website for licensed regional carriers in your ZIP code.

Frequently Asked Questions About the Best Car Insurance in the USA

Q: What is the best car insurance company in the USA in 2026?

A: Travellers ranks first overall in 2026 with a 4.8 out of 5 score, leading in 8 of 11 driver categories. GEICO offers the lowest rates at $98/month for full Coverage. Amica delivers the best customer service with a perfect 5/5 experience rating. The best company for you depends on your driver profile, city, and coverage priority — use the 4-Filter Framework to identify your personal best match.

Q: How do I find the best car insurance for young drivers in 2026?

A: State Farm charges $208/Month for a 16-year-old — the lowest among major national carriers, compared to Progressive’s $467/month and Farmers’ $452/month for the same profile. Young drivers should also explore State Farm’s Steer Clear program, which adds discounts for drivers under 25 who complete safe-driving coursework. Always compare one regional carrier alongside national brands — regional insurers often price young drivers more competitively in specific states.

Q: What is the best car insurance in New York in 2026?

A: In New York, GEICO and Progressive offer the cheapest rates among major national carriers in 2026. NYCM Insurance offers competitive regional rates for New York residents. Always quote by exact ZIP code — rates in Brooklyn can be twice those in Manhattan for identical Coverage. Drivers with fewer than 7,500 miles/year may benefit from pay-per-mile options like Metromile.

Q: What is the best car insurance in California in 2026?

A: GEICO and CSAA (AAA) offer the cheapest car insurance rates in Los Angeles and most of California in 2026. California bans the use of credit scores and gender in rate-setting, so your ZIP code and driving record carry the most weight. Mercury Insurance offers strong regional pricing in Southern California. Drivers with fewer than 7,500 miles/year should ask explicitly about low-mileage discounts — California law requires insurers to offer them.

Q: Is the best car insurance always the cheapest option?

A: No — the best car insurance delivers the highest value per dollar, not the lowest absolute premium. Minimum Coverage averages $800 annually nationally, but leaves drivers financially exposed in severe accidents — making it the wrong choice for most drivers with assets to protect. The best car insurance matches your coverage level to your actual financial risk, not just your monthly budget.

Q: What are the biggest mistakes people make when choosing car insurance?

A: The four most costly mistakes are: choosing by brand recognition instead of data, accepting a quote without checking AM Best rating, failing to re-quote after life changes, and ignoring the NAIC complaint index. Any single mistake can cost $400–$1,500 per year in either overpayment or claims difficulty. The 6-step process in this article addresses all four.

Q: How do I compare the best car insurance companies step by step in 2026?

A: Apply the 4-Filter Framework first: identify your driver type, state/city, coverage priority, and financial risk tolerance. Then run at least 5 quotes, including one regional carrier, with identical coverage limits across all quotes. Request every applicable discount before accepting. Verify each insurer’s AM Best rating and NAIC complaint index before signing. Set a renewal reminder 30 days before your policy expires. Repeat annually — the best insurer for your profile in 2025 may not be the best in 2026.

Q: What is the best car insurance in Dallas and Houston in 2026?

A: In Dallas, Travellers offers the strongest combination of price ($138/month estimated) and overall rating. Texas Farm Bureau offers the lowest rates for eligible members at approximately $129/month. In Houston, GEICO and Travellers compete most aggressively, with Progressive’s Snapshot telematics program offering additional savings for safe drivers. Both cities benefit from including Texas Farm Bureau in your comparison, as it consistently undercuts national brands for eligible Texas residents.

Conclusion

The bottom line about the best car insurance is simpler than it looks.

No single insurer wins for every driver. The best car insurance in the USA in 2026 is the one that combines financial stability, competitive pricing for your specific profile, and a claims track record you can verify — not the one with the most advertising.

Here are the three things to do this week:

Run the 4-Filter Framework — identify your driver type, city, coverage priority, and risk tolerance before opening a single comparison site.

Check AM Best and NAIC — verify your top two candidates at ambest.com and naic.org before accepting any quote.

Include one regional carrier — search your state’s Department of Insurance website for licensed regional insurers and add the top one to every quote comparison.

The best car insurance decision is a structured process, not a gut feeling. Drivers who treat it as a process pay hundreds of dollars less per year than those who default to the first recognizable brand.

Start with the 4-Filter Framework. It takes 5 minutes and changes every comparison you run after it.

About the Author Jahedul is a CFP®-certified financial writer with 11 years of experience covering personal finance, auto insurance, and consumer protection for readers across the USA, UK, and Canada. She specializes in translating insurance pricing systems into clear, actionable frameworks that help everyday drivers make better coverage decisions.

Disclaimer: This article is for informational purposes only and does not constitute financial or insurance advice. Please consult a licensed financial advisor or insurance professional before making any decisions.